Başkan Murat Çetinkaya'nın "Makroekonomik Görünüm ve Para Politikası" Başlıklı Konuşması (İngilizce) (Londra)

Dear Participants,

My speech will try to elaborate on the recent macroeconomic outlook, monetary policy framework and the coordinated policy actions to support the fundamentals of the Turkish economy.

1. Macroeconomic Outlook

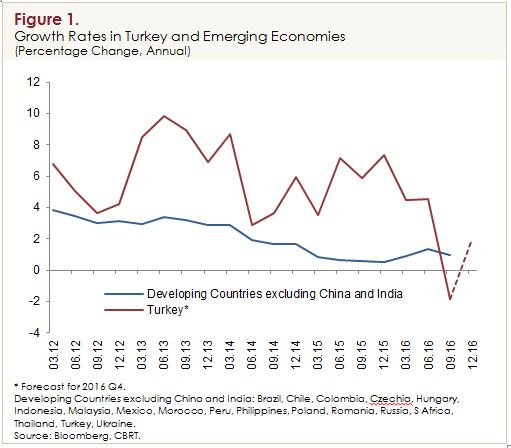

Turkish economy was hit by concurrent shocks in recent years. Geopolitical tensions, global shocks, security related issues and a failed coup attempt have created significant policy challenges. Despite the intensity and size of the shocks in recent years, the growth rate has been quite robust until recently, outpacing emerging market average by a large margin (Figure 1). The resilience of growth in recent years can be attributed to factors such as prudent macroprudential policies reducing the sensitivity of economic activity to capital flow volatility, dynamic domestic market, market flexibility of exports, and the fall in energy prices.

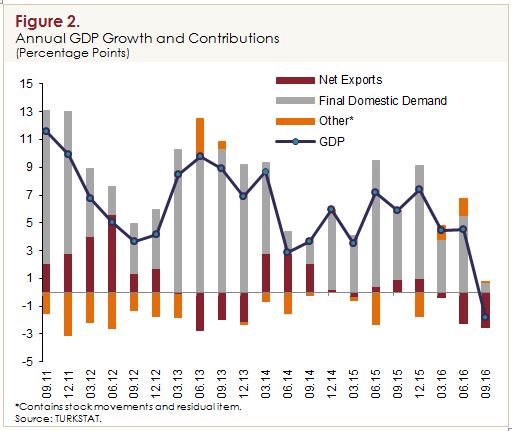

However, the growth has posted a marked slowdown in the third quarter of 2016, following the failed coup attempt. GDP has contracted year-on-year terms for the first time since the global financial crisis. The weakness in economic activity was driven by a sharp fall in domestic demand and the sizeable drop in tourism revenues (Figure 2).

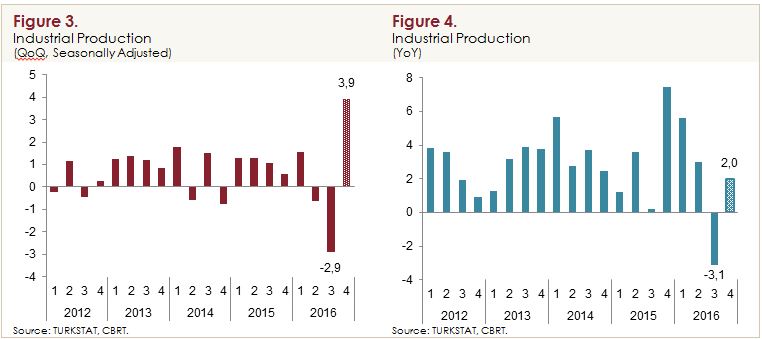

One important question was whether the third quarter would stay as a temporary slump or more slowdown was on the way. Recent indicators suggest that the contraction in economic activity was short-lived. We observed a rebound in the final quarter of the year as depicted by the rapid recovery in the industrial production (Figure 3). Some of the recovery can be attributed to corrections due to technical factors such as shifting holidays and associated changes in the number of working days. Therefore, looking through temporary factors, we assess that economic activity has expanded at a moderate pace during the final quarter of 2016 (Figure 4). We expect that the recovery will continue to be mild and gradual throughout 2017, which will leave the output gap at the negative territory. Main drivers of growth this year will be public investment expenditures and exports.

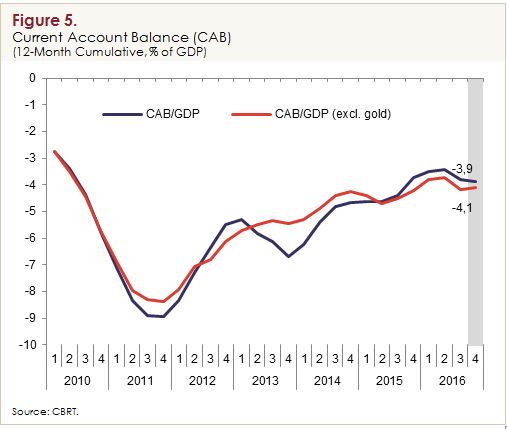

On the external side, I would like to note that the Turkish economy has been undergoing a persistent rebalancing process in recent years. Current account deficit has come down from a peak of 9 percent to less than 4 percent recently (Figure 5). Although improvement was partly reversed after mid-2016 due to sharp fall in tourism revenues, we expect the deficit to continue to shrink gradually throughout 2017. Main drivers of the improvement in the current account balance will be the recovery in exports and the weaker imports due to real exchange rate.

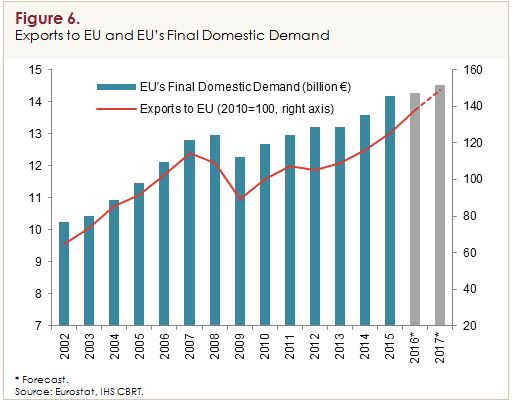

We think that exports will be one of the main drivers of growth in 2017. The main contribution to exports is expected from the European demand. Turkish exports are highly sensitive to the demand from Europe which constitute more than half of our total exports. Latest projections suggest that EU demand will continue to support Turkish exports in the forthcoming period (Figure 6). Moreover, recently improved relations with our neighbors have also started contributing to the export growth again after a long stagnation period. Recently, there is some slight recovery in exports to our main major trading partners such as Iraq and Russia. The recovery process is expected to continue throughout 2017. Overall, we anticipate a sizeable contribution from exports to growth in 2017.

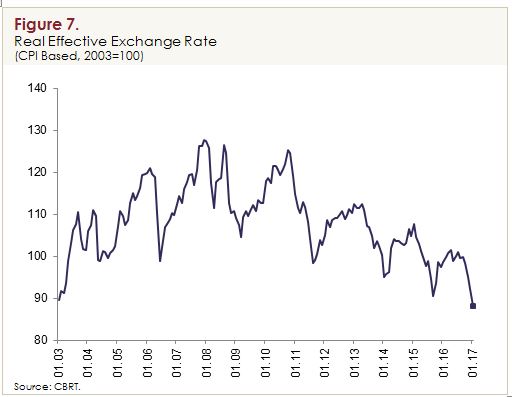

Another factor that will lead to an improvement in exports and current account balance is the depreciation of the Turkish lira. As of January, the real effective exchange rate index has fallen to 88.2, which is the historically lowest level in the past 15 years (Figure 7). The most recent data show that export growth has been outpacing import growth and we expect this picture to become more evident during the first half of 2017.

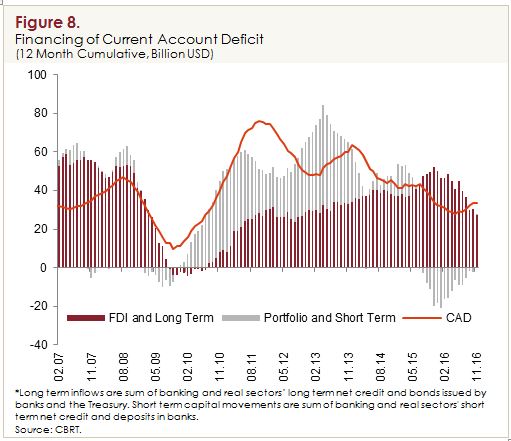

Regarding external finance, current account deficit is financed predominantly by FDI flows and long term borrowing (Figure 8). Most recently, we still see a sizeable contribution from FDI and long term borrowing by banks and non-financial corporates, whereas portfolio inflows have been relatively weak. The share of long term debt in total debt has been increasing steadily. The banks and firms are able to roll their debt comfortably, and the roll-over ratios are still above 100%.

Dear Participants,

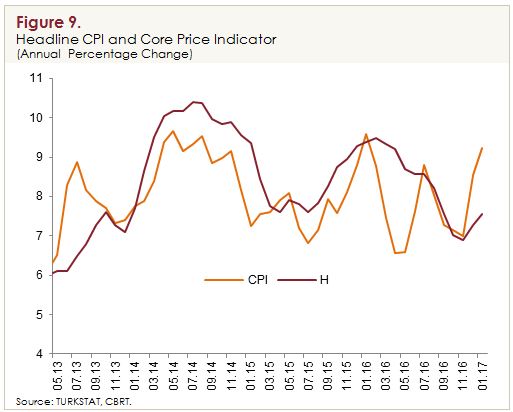

Now, let me turn to inflation developments. In the past few months, we have observed a marked increase in the CPI inflation, while the core inflation indicators have shown a milder upward movement (Figure 9). The main driver of inflation in the most recent data was unprocessed food prices, most of which can largely be attributed to adverse weather conditions. Tax hikes and the exchange rate pass-through have also had a visible impact on inflation in recent months. The rise in core inflation was relatively subdued, despite the sharp exchange rate depreciation. Although recently observed pass-through seems lower than historical estimates due to subdued demand conditions, exchange rate movements still pose upside pressures on inflation.

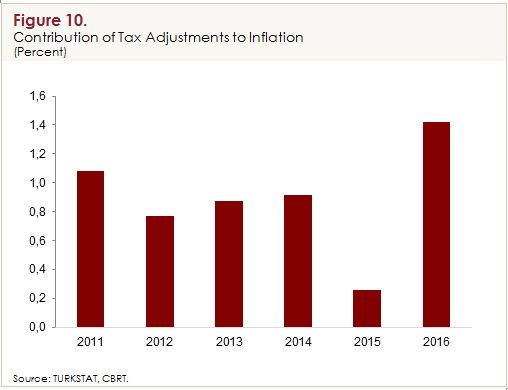

Going ahead, the lagged pass-through impact and the base effects resulting from previous year’s food price volatility will continue to weigh on inflation. On the other hand, the impact of tax adjustments on CPI inflation is likely to fade away throughout 2017, given the government’s clear statement of no additional tax hikes in 2017 (Figure 10).

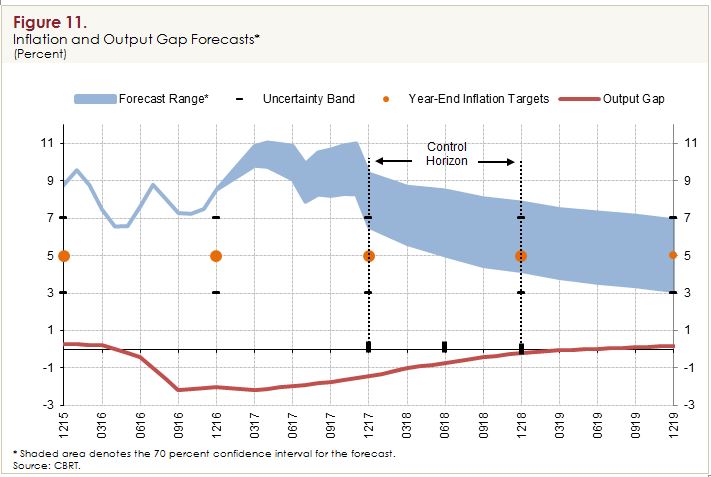

Our recent Inflation Report provides the updated inflation and output gap forecasts. We have revised the output gap on the downside, whereas short-term inflation projections have been revised upwards. Disinflationary impact of weaker economic activity was more than offset by the exchange rate pass-through effect for the near term forecasts. Inflation is expected to further edge up in the short term before gradually coming down to 8 percent at the end of the year (Figure 11). Tighter monetary policy along with more coordinated fiscal policy conduct should contain the second round effects of the cost-push developments. Accordingly, we see inflation at 6 percent at the end of 2018 as the pass-through effect diminishes over time.

2. Monetary Policy

Dear Participants,

I will devote the final section of my speech to the policy response to recent developments. The main focus will be on the CBRT policies, but at the end I will also try to elaborate briefly on how the other policies on the macroprudential and fiscal side are coordinated to address the associated trade-offs.

Central Bank of Turkey has taken a series of steps in 2016 to simplify the monetary policy framework. The intention was to gradually withdraw from the multiple policy rate setup in order to improve the effectiveness of monetary policy and enhance policy predictability. We were able to stick to our plan until the end of the year, even after the currency pressures increased after the US elections. In fact, our interest rate hike in November was the first conventional interest rate response since 2008.

However, the situation in early January necessitated an alternative approach. We have witnessed price movements in the FX market which could not be justified by economic fundamentals. The volatility increased sharply, which could be detrimental for both price and financial stability. The response to this unprecedented episode had to be swift, strong, and targeted. Given the significant downside risks to the economic activity and the credit supply, we decided to implement a monetary tightening which would strongly address the direct cause of the problem, with less significant implications on the real side of the economy. To this end, we have tightened the liquidity supply and induced a sharp increase in the short term interest rates at the interbank market. Moreover, to further strengthen our control on the short-end of the yield curve, we have devised a new tool which is practically equivalent to a currency swap. This facility not only sets a benchmark for the price formation in the FX market but also supplies temporary FX liquidity to the market when needed.

At our January MPC meeting, we have increased the overnight repo and late liquidity window rates, delivering a strong monetary tightening in order to contain the deterioration in the inflation outlook. The MPC statement underlined that the CBRT will continue to use all available instruments in pursuit of the price stability objective.

We have also stated that inflation expectations, pricing behavior and other factors affecting inflation will be closely monitored and, if needed, further monetary tightening will be delivered. Moreover, the statement signaled that necessary liquidity measures will be taken in case of unfounded pricing behavior in the foreign exchange market that cannot be justified by economic fundamentals.

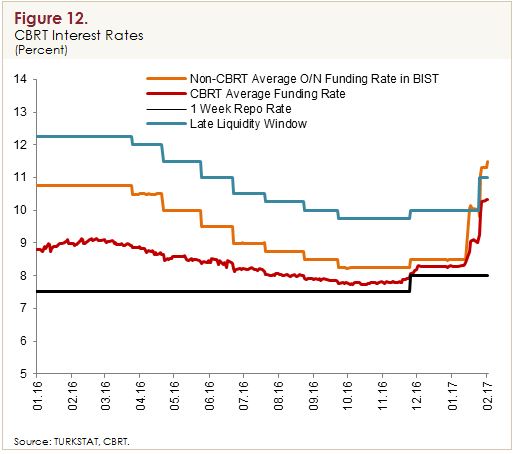

The figure depicts the two main interest rates that matters most for the monetary transmission mechanism (Figure 12). The first one is the cost of central bank funding (shown by the red line), which recently has increased by 200 basis points to around 10.3 percent. The second one is the interbank rate (orange line), which has sharply moved up and have been consistently close to 11 percent since our latest MPC meeting. These two rates clearly indicate that monetary policy has been tightened to a great extent.

I would like to underline that the recent policy we have been implementing is not equivalent to the previous discretionary monetary policy under a flexible corridor framework where the policy stance shifted at daily and weekly frequencies. This is a clear and stable policy tightening which will be preserved until we see a considerable improvement in medium term inflation dynamics.

The significant tightening in the monetary policy stance can also be observed directly by looking at the yield curves. The left side figure shown below compares the most recent yield curve with the one materialized in early January, right before the CBRT response (Figure 13). It is clear that the short-end has shifted up and the longer-end has fallen, which is a typical response after a credible monetary tightening. As another indicator of the monetary tightening in time dimension, the right side figure below shows the evolution of the slope of the yield curve at the cross currency swap market, which also clearly reveals a flattening in the yield curve (Figure 14).

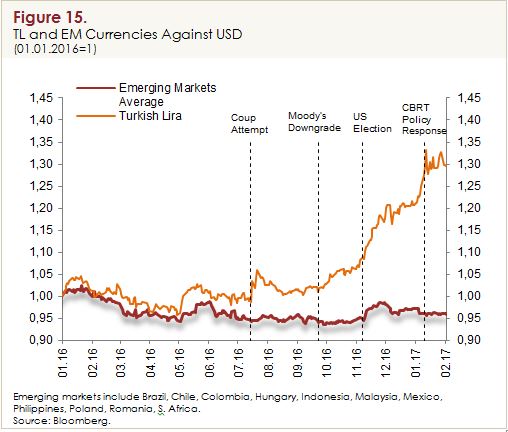

Were these policies effective? More time is needed to assess the ultimate impact, but the initial response is encouraging. Turkish lira, which has depreciated relative to peer currencies in the second half of 2016, has stabilized after the policy tightening, partly containing the upside risks on the inflation outlook (Figure 15).

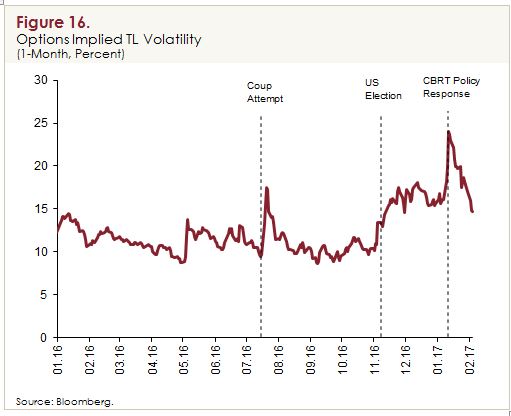

The policy we adopted has been also effective on the volatility indicators. The last figure I would like to show you pertains to the volatility in the FX market (Figure 16). As you can see, the implied volatility of Turkish lira has moved up sharply in early-January, but eased significantly after the implementation of the recent CBRT measures.

Dear Participants,

Let me wrap up my speech by highlighting the value of close policy coordination. Turkey has faced a series of significant shocks in the past years. Most recently, the slowdown in the economic activity, tightening in financial conditions, sharp currency depreciation, and rising inflation have necessitated a coordinated action by all relevant authorities.

Central Bank has mainly focused on inflation and FX developments during this period. We used our rich toolkit to tighten monetary policy, but at the same time provided liquidity support to FX market through reserve requirements and other tools.

As part of the coordinated policy mix, other authorities have taken a series of measures to support the credit channel and economic activity. In order to stimulate the loan supply and demand, the bank regulation authority has released some of the buffers accumulated in recent years, including the maturity restrictions and loan-loss provisions. The government has announced a stimulus package to contain a possible adverse feedback loop between economic activity and loan supply. To this end, collateral conditions were eased for corporates, several incentives were provided to stimulate investments and exports, direct support for SME loans were provided through government guarantee schemes and loan restructuring processes. Most recently, tax cuts have been introduced for certain durable products to support demand and production without generating inflation. Moreover, as a reflection of the enhanced fiscal-monetary policy coordination, the finance ministry announced clearly that no tax hikes are envisaged in 2017.

We anticipate that these concerted efforts will not only bring inflation gradually towards our medium term target of 5 percent but also support the economic recovery in the forthcoming period.

Thank you for your attention.