Governor Başçı's Speech in Press Conference for the Presentation of the Inflation Report-IV (Ankara, 26/10/2011)

Distinguished Guests,

Unlike former press conferences held to present inflation reports, today I would like to start my presentation by explaining a five-point action plan entailing price stability, interest rate policy, foreign exchange reserves policy, required reserves policy and financial stability.

We are living through a period marked by global developments that call for taking timely, and if necessary, daily counter-cyclical measures against capital flows. Therefore, with the Monetary Policy Committee’s decision of October 20, 2011 we achieved the flexibility needed to effectively implement the twoobjective and three-instrument monetary policy on a daily basis. After briefly mentioning the outlook for our primary objective of price stability, I will summarize how and in which direction the three instruments will be employed from now on. Lastly, I will also briefly talk about the positive impacts of decisions that have already been or will be taken regarding financial stability. Firstly, I will talk about price stability. We expect inflation to rise significantly in the upcoming months due to recent excessive depreciation of the Turkish lira, the base effects from unprocessed food prices and the recent adjustments in administered prices. I would like to reiterate that we will not allow these developments to affect medium-term inflation expectations and the mediumterm inflation outlook adversely. Indeed, we have already started the necessary monetary tightening to keep inflation under control and to ensure that inflation realizations remain in line with the target set for 2012. Details on this issue can be found in the Inflation Report that I will summarize shortly.

Secondly, I will talk about our interest rate policy. After the last Committee meeting, banks’ funding costs from the Central Bank were set within the interest rate corridor, in other words, between 5.75 and 12.5 percent on average, or at a level that the Central Bank considers appropriate. In cases where funding is effected at 12.5 percent, the Central Bank will meet banks’ demand with no upper limit and against eligible collateral. Tightening or easing to be achieved via the funding channel will be implemented even on a daily basis depending on the course of economic and financial developments. In the event that risks to price stability are observed, the Central Bank will allow banks’ overnight borrowing rates to hover around 12.5 percent for some time.

Thirdly, I will provide you with some information about our reserve requirement policy. Depending on the outcome of the EU Leaders Summit and the foreign markets’ perception of this outcome, the Central Bank may introduce a limited reduction in the Turkish lira required reserve ratios if deemed necessary. Moreover, we may also allow holding of up to 40 percent of Turkish lira reserve requirements in foreign currency. Meanwhile, technical studies are underway for enabling a facility that allows holding of 10 percent of Turkish reserve requirements in gold. We believe that these three decisions will have positive impacts on our banks, especially through the cost channel. Consequently, the Turkish lira liquidity to be supplied to the market will significantly and permanently diminish the funding needs of our banks; thus, favorably affecting the banking sector via the liquidity channel as well.

Now, I would like to talk about our reserve policy. Following the enabling of the facility that allows holding precious metal deposit accounts and a part of FX reserve requirements in the form of "standard gold", starting from October 28, 2011, we expect to see a rise in Central Bank gold reserves from for the first time since 1991. Central Bank’s gold reserves may continue to increase once it holding of Turkish lira reserve requirements in the form of gold is also allowed. The Central Bank purchased USD 26 billion-worth of foreign currency between August 2009 and July 2011. These purchases were primarily aimed at prudently supplying FX liquidity to our financial system, when needed, in order to support both price stability and financial stability. Accordingly, should unhealthy price formations arise due to loss of depth in the FX market, we can resume FX selling auctions or directly intervene in the FX market without undermining the basic principles of the floating exchange rate regime. In addition, depending on the global economic developments, we may resume intermediary activities in our FX Deposit Market with the aim to enhance FX liquidity flow in the interbank FX market.

Lastly, I will briefly mention the issue of financial stability. We can summarize the core objective of the policies we have been implementing since November 2010 as slowing down the excessively rapid growth of the private sector’s external liabilities and improving the quality of these liabilities. Accordingly, the downward trend in the seasonally adjusted month-on-month current account deficit, which started in July 2011, will continue in the final quarter after a pause in September 2011. The steady rise in the shares of direct foreign investments and long-term borrowing in the financing of the current account deficit continues. We believe that further slowing down of the current pace of growth, especially in consumer loans, in the rest of the year would contribute to the sustainability of the rebalancing of domestic and external demand. Thus, the rise in the private sector’s propensity to save in Turkey will ensure a more rapid and sound correction in the current account deficit. In the upcoming period, effective liquidity management through the interest rate corridor will become an important policy instrument that will also contribute to financial stability.

Distinguished Members of the Press,

Now, in order to provide more detailed information on the price stability pillar of the framework that I have just mentioned, I would like to share with you the main messages of the October Inflation Report.

The Report typically summarizes our evaluations on macroeconomic developments and presents our revised medium-term inflation forecasts, along with our monetary policy stance. In addition to the main sections of the Report, we have provided nine boxes that analyze various topics. These boxes, like usual, evaluate the findings of studies on some interesting current topics. For instance, we have a box on the crisis and debt sustainability in the Euro area. Also, we have boxes that elaborate two popular topics that have been occupying the top of the agenda for some time. In one of these boxes, the method of taxing tobacco products and its impact on consumer prices is analyzed, while in the second box, we share our current forecasts on exchange rates and import price pass-through. You can see titles of other boxes on the other slide. All of them contain informative analyses on the Turkish economy. These boxes will be published shortly on our website; I recommend you to read them.

Distinguished Members of the Press,

Global economic developments have been influential on our policies for quite a long time. Therefore, in the first part of my speech, I would like to continue with a brief summary of these developments.

In the third quarter of 2011, mounting concerns regarding sovereign debt sustainability across the euro area, coupled with the slower-than-expected recovery in U.S. real estate and labor markets intensified the downside risks regarding global economic activity. Accordingly, global economic activity forecasts were revised downwards and expectations for a further delay in the normalization of monetary policy in advanced economies grew stronger. Mounting uncertainties regarding the global economy and the deterioration in risk appetite led to capital outflows from emerging economies. This outlook not only fed into short-term inflationary pressures in emerging economies, but also highlighted concerns over growth and financial stability.

1. Monetary Policy Developments and Monetary Conditions

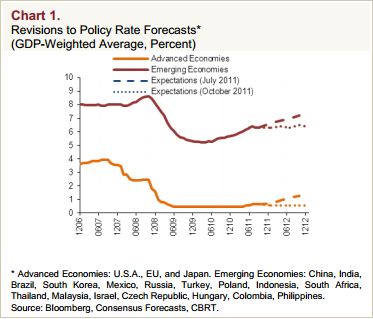

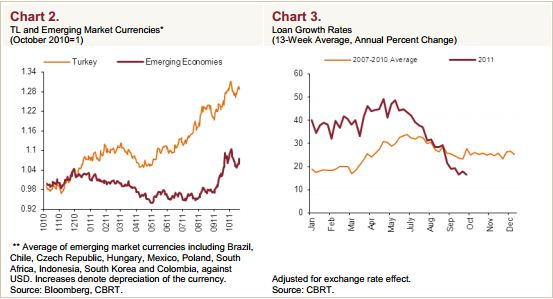

The policies that we, as the Central Bank of the Republic of Turkey (CBRT), have been implementing since end-2010, aimed at gradually rebalancing the economy towards a robust growth composition without hampering the mediumterm inflation outlook. Accordingly, we pursued policies to prevent excessive deviation of exchange rates from economic fundamentals in either direction, while also taking the necessary measures with the support of other institutions to ensure reasonable levels in loan growth rates (Chart 2 and 3).

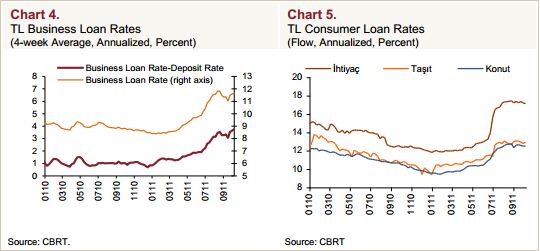

As a consequence of measures taken by the Central Bank and the Banking Regulation and Supervision Agency (BRSA), loan rates continued to rise in the third quarter (Charts 4 and 5). A marked slowdown is observed in credit growth owing to the lagged effects of measures taken and a deceleration in economic activity. Despite the role of seasonal factors, this slowdown is more apparent compared to that of recent years (Chart 3). Accordingly, the exchange-rateadjusted annual credit growth rate is expected to converge at around 25 percent by year-end, as envisaged.

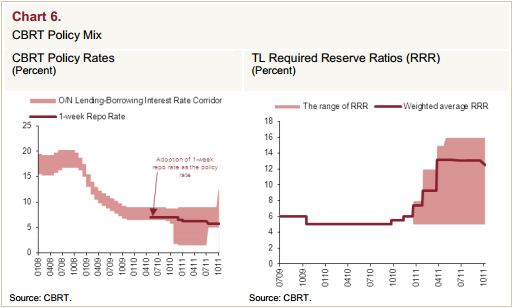

In the baseline scenario presented in the July Inflation Report, global economic activity was assumed to continue to improve gradually; however, it was also highlighted that downside risks on the global economy were growing stronger. Indeed, right after the publication of the Report, risk perceptions deteriorated rapidly and debt problems in the euro area further intensified changing the baseline scenario. In response, we introduced a comprehensive package of measures to contain the potential adverse effects of these developments on financial stability and economic activity. The objective of these measures was to supply liquidity to markets in a timely, controlled and effective manner in the event of financial turmoil that may be driven by developments in the global economy. Moreover, we opted for a modest cut in the policy rate in order to contain the risk of recession in domestic economic activity that may be posed by escalating global economic problems. Moreover, Turkish lira required reserve ratios were adjusted in order to extend the maturities of liabilities of the banking system (Chart 6). The mounting uncertainties facing the global economy since the July Inflation Report and accelerating capital outflows from emerging economies called for a series of measures intended to contain fluctuations in the foreign exchange market.

Distinguished Guests,

Ongoing deterioration in the global risk appetite, which started in August, has led to excessive depreciation of the Turkish lira. The accumulated depreciation of 30 percent since November 2010 started to pose risks on the inflation outlook. Moreover, in October, adjustments made to administered prices, which were far beyond the assumptions of the July Inflation Report, necessitated a sizeable upward revision of short-term inflation forecasts. At this point, I would like to underline that we would not allow the medium-term inflation expectations and outlook to be affected by these developments, and we will take all necessary policy measures. The policy measures that I mentioned earlier in my speech and the Committee decision of October stipulating a significant increase in the overnight lending rate should be viewed from this perspective (Chart 6).

2. Inflation and Monetary Policy Outlook

Distinguished Members of the Press,

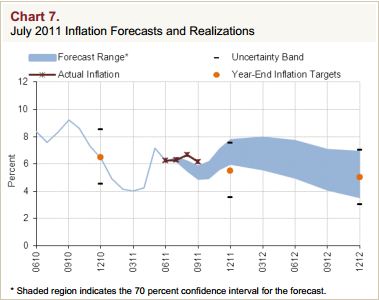

I would now like to discuss the macroeconomic outlook and the assumptions underlying our forecasts. First of all, I will summarize the recent inflation developments and then I will compare the short-term forecasts we announced in July with data realizations in the third quarter. In the third quarter, prices of core goods posted a more-than-envisaged increase amid excessive depreciation of the Turkish lira. The annual rate of change in food prices declined significantly due to the base effect in unprocessed food prices. As seen on the slide, inflation followed a flat course during the third quarter as these two effects largely offset each other (Chart 7). However, exchange rate developments ended up being more dominant which led inflation to exceed the forecast range presented in the July Inflation Report.

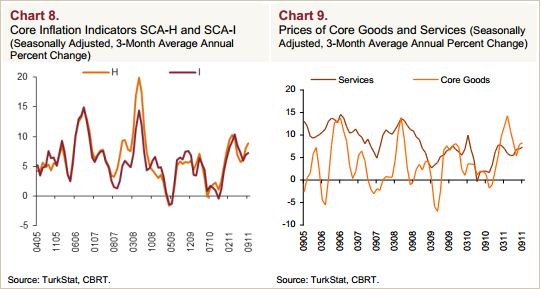

In the third quarter, exchange rate developments led to an increase in the underlying trend of core inflation indicators as well (Chart 8). This was mainly triggered by the increase in prices of core goods, while the underlying trend of services inflation remained relatively modest (Chart 9).

Distinguished Guests,

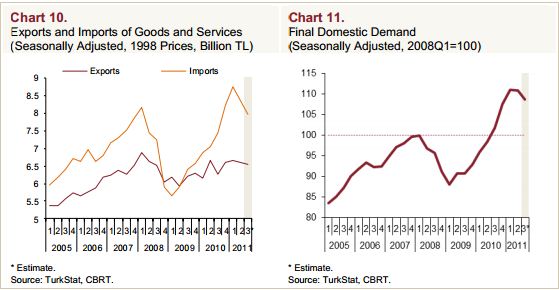

Gross Domestic Product (GDP) data indicated more robust economic activity in the second quarter of 2011 compared to the outlook presented in the July Inflation Report. Therefore, the output gap estimates of this period were revised upwards. Private sector consumption and investment expenditures became the main drivers of growth in this period. While exports followed a weak course amid developments in the global economy, imports recorded a significant decline following the slowdown in domestic demand due to the policy measures adopted. Thus, the net external demand made a positive contribution to growth on a quarterly basis for the first time after a long stretch. In other words, the composition of growth started to change in the desired direction (Chart 10).

Owing to the lagged effects of the contractionary reserve requirement and liquidity policies, domestic demand continued to lose pace in the third quarter. Also, due to measures taken by the Banking Regulation and Supervision Agency (BRSA) and the tight fiscal policy stance, domestic demand growth was brought to a sustainable level in the third quarter. In this period, credit, production and sales data, as well as confidence indices, indicated ongoing loss of momentum in private consumption demand. In this context, the outlook for the third quarter was based on an ongoing slowdown in domestic demand (Chart 11).

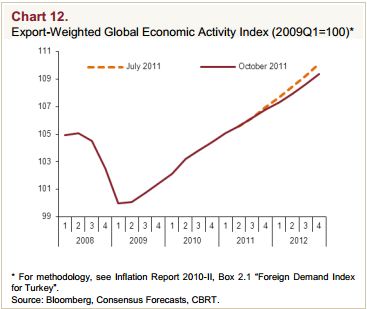

Driven mainly by advanced economies, global growth forecasts were subject to substantial downward revisions in the third quarter. In this respect, projections for Turkey’s export-weighted global growth index point to a weaker medium term outlook compared to the previous period (Chart 12). Therefore, forecasts were based on an outlook of weaker external demand compared to the previous period.

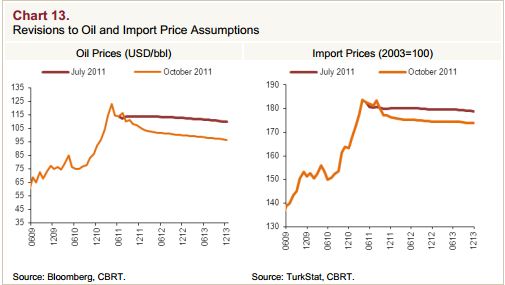

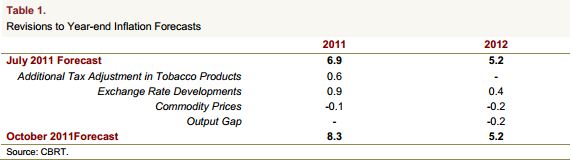

Consequently, the output gap was revised upwards for the short-term and downwards for the medium term. Moreover, assumptions on oil and other commodity prices were revised slightly downwards (Chart 13). You can see the effect of these revisions on 2011 and 2012 year-end inflation forecasts (Table 1).

Esteemed Guests,

In the July Inflation Report, the price increases in tobacco products were assumed to be consistent with the inflation target, adding approximately 0.3 percentage points to inflation. However, considering recent developments, the estimated contribution of price increases of tobacco products to inflation is revised upwards to 0.9 percentage points. This has led to an increase in short term inflation forecasts by 0.6 points (Table 1).

The assumptions about fiscal policy used for medium-term forecasts were based on the outlook presented in the Medium Term Program (MTP). Therefore, the baseline scenario envisages that the ratio of primary expenditures to GDP would gradually be reduced from 2012, the public debt-toGDP ratio would continue to fall, and the risk premium would remain broadly unchanged. Moreover, tax adjustments and administered prices are assumed to be consistent with inflation targets and automatic pricing mechanisms.

Distinguished Members of the Press,

As I have already stated, since the publication of the July Inflation Report, emerging economies have faced rapid capital outflows due to the deteriorating risk appetite. In this respect, excessive depreciation in the Turkish lira has become more evident. This development, coupled with the increase in prices of administered goods, has raised the risk of deterioration in pricing behavior. We responded to these developments strongly by increasing our overnight lending rate markedly in our October meeting (Chart 6). We expect monetary tightening to contain inflationary pressures in the period ahead. However, inflation is forecasted to increase significantly in the short term with the contribution from low base effects in unprocessed food prices.

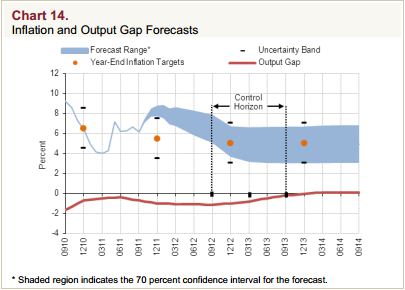

Assuming that the annual rate of credit growth decelerates gradually, and monetary conditions are tightened significantly in the final quarter in line with policy measures taken in October, inflation is expected to be, with 70 percent probability, between 7.8 and 8.8 percent with a mid-point of 8.3 percent at the end of 2011, and between 3.7 and 6.7 percent with a mid-point of 5.2 percent at the end of 2012. Inflation is expected to stabilize around 5 percent in the medium term (Chart 14).

I would like to reiterate that any new data or information regarding the inflation outlook might lead to a change in the monetary policy stance. Therefore, assumptions regarding the monetary policy outlook underlying the inflation forecast should not be perceived as a commitment on behalf of the CBRT. In sum, short-term inflation forecasts were revised on the upside mainly due to exchange rate developments and hikes in administered prices. I would like to underscore that these factors reflect a movement in relative prices rather than a permanent increase in inflation, as the monetary tightening envisaged in the last quarter in the context of the CBRT’s recent strong policy reaction will prevent second round effects.

Distinguished Guests,

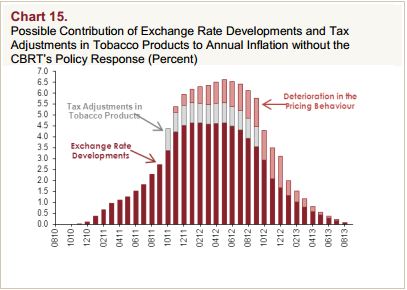

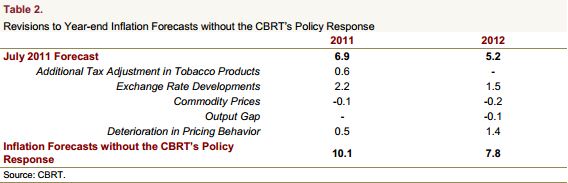

I would like to highlight once more that the recent tightening in the CBRT’s policy stance aims mainly to prevent deterioration in inflation expectations triggered by inflationary pressures from the exchange rate. At this point, it is important to ask a counterfactual question: what would the path of inflation have been had the CBRT not reacted? To provide more guidance on this matter, I would like to draw your attention to the chart (Chart 15). The chart depicts accumulated price increases resulting from exchange rates and administered price developments, in the case of no reaction by the CBRT. Accordingly, we estimate that the contribution of these developments to inflation would have reached 6 percentage points, had the CBRT not taken any policy measures.

In this scenario, consumer inflation reaches double digits at 10.1 percent, owing mainly to the excessive depreciation of the Turkish lira, also coupled with the effect of the deterioration in inflation expectations (Table 2). Therefore, given the backward looking pricing-behavior in the services sector, inflation would hover at elevated levels for an extended period of time. This would lead to a deterioration in inflation expectations, and risk the hard-earned recent achievements on the path to price stability. In such a case, bringing inflation back to reasonable levels would be more costly. In order to prevent such adverse developments, the CBRT intervened actively in the foreign exchange market; and in line with its primary objective of price stability, responded boldly by increasing overnight lending rates significantly. Besides, we have explicitly stated that the CBRT, in line with the strategy announced today, will not allow exchange rates to deviate from economic fundamentals, nor will it allow a deterioration in price stability and financial stability. I would like to reiterate that various measures will continue to be taken in the forthcoming period, in order to ensure price stability.

3. Risks and Monetary Policy

In the last part of my speech, I would like to mention risks regarding the inflation outlook and how the monetary policy will be shaped should these risks materialize.

The fact that inflation will hover above the target in the short term poses risk to inflation expectations and price setting behavior. Accordingly, as of October, the CBRT has adopted a policy stance aimed at eliminating these risks. These risks will be closely monitored and the necessary measures will be taken to avoid deterioration in the medium-term inflation outlook.

Medium term projections assume that the global outlook will remain weak for a long period, but the situation will not worsen further. Nevertheless, uncertainties regarding the global economy continue to be of significant concern. Especially, mounting problems regarding the sovereign debt of euro area economies continue to pose downside risks on the global economy. Concerns regarding the debt sustainability of euro area economies have further increased since the publication of the July Inflation Report, exacerbated by the concerns of a possible contagion to the region’s banking sector. In this context, the CBRT will continue to monitor global economic developments closely and will take the required measures promptly to maintain stability in domestic financial markets. While formulating the monetary policy, we will continue to monitor fiscal policy developments closely as well. In this respect, our forecasts presented in the baseline scenario take the Medium Term Program as given and thus assume that fiscal discipline will be maintained. A revision in the monetary policy stance may be considered, should the fiscal stance deviate significantly from this framework and consequently have an adverse effect on the medium-term inflation outlook.

In the period ahead, monetary policy will continue to focus on price stability while preserving financial stability as a supporting objective. To this end, the impact of the macroprudential measures taken by the CBRT and other institutions on the inflation outlook will be carefully assessed. Strengthening the commitment to fiscal discipline and the structural reform agenda in the medium term would support the relative improvement of Turkey’s sovereign risk and thus, facilitate macroeconomic and price stability. Sustaining the fiscal discipline will also provide more flexibility for monetary policy and support social prosperity by keeping long-term interest rates permanently at low levels. In this respect, I would like to conclude my remarks by underlining that timely implementation of the structural reforms envisaged by the new Medium Term Program remains to be of the utmost importance.

Thank you for your participation.