Governor Başçı's Speech in Press Conference for the Presentation of the Inflation Report-III (Ankara, 28/07/2011)

Distinguished Members of the Press, Esteemed Guests,

Welcome to the press conference held to convey the main messages of the July 2011 Inflation Report.

The Report typically summarizes the economic outlook underlying monetary policy decisions, shares our evaluations on global and domestic macroeconomic developments and presents our medium-term inflation forecasts, which have been revised in view of the last quarter developments, along with our monetary policy stance. As usual, in addition to the main sections of the Report, we have also prepared additional boxes analyzing special topics. You may see the titles of these eleven boxes, all of which containing useful analyses regarding the Turkish economy. They will be published shortly on our website; I recommend that you read them.

Distinguished Members of the Press,

Global economic developments have been influential on our policies for a long while. This is likely to persist for an extended period. Therefore, in the first part of my speech, I would like to very briefly summarize these developments.

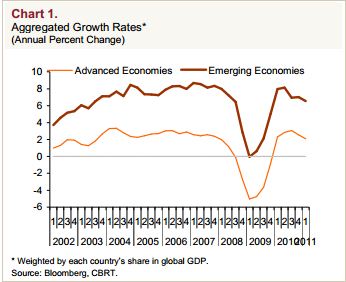

Global economic growth slowed down in the second quarter of 2011, while advanced and emerging economies continued to grow at different paces (Chart 1). Being mainly driven by increasing concerns regarding sovereign debt sustainability problems across the euro area, especially in Greece, downside risks to global economic growth were more apparent in this period. The slowerthan-expected recovery in the U.S. labor market and the ongoing problems regarding public debt management were also among the agenda items. Accordingly, there have been growing expectations that the normalization of monetary policy in advanced economies would be further postponed. In contrast, emerging economies faced with inflationary pressures arising from strong domestic demand and elevated commodity prices continue to tighten monetary policy while resorting to macroprudential measures to contain the adverse effects of global imbalances on their domestic markets.

1. Monetary Policy Developments and Monetary Conditions

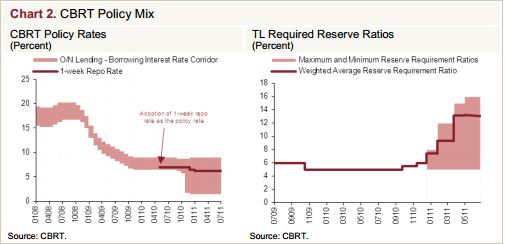

As you have been following closely, in line with the exceptional global economic conditions we have going through; we, as the Central Bank of the Republic of Turkey, have developed a different approach with regard to monetary policy. In order to restrain the macro financial risks in the domestic economy posed by short-term capital inflows, rapid credit growth and the widening current account deficit, we have started to implement a new policy strategy by the end of 2010. The new policy approach preserves the main objective of achieving and maintaining price stability, while also observing financial stability as a supportive objective. In this context, in addition to policy rates, complementary tools such as reserve requirement ratios and the interest rate corridor are jointly utilized.

In order to contain risks associated with diverging domestic and external demand and short-term capital inflows, we have kept policy rates at low levels, while enforcing monetary tightening through reserve requirement hikes since the last quarter of 2010. This strategy aims to rebalance economic growth without deteriorating the medium term inflation outlook. Accordingly, by gradually raising the reserve requirement ratios as of end-2010, we assumed a more cautious position in our monetary stance (Chart 2).

Observing the moderating domestic economic activity and mounting uncertainties regarding the global economy, we have not changed the policy rate and the Turkish lira reserve requirements since the publication of the April Inflation Report. However, recent developments brought us one step closer to the downside risk scenarios mentioned in the April Inflation Report. Accordingly, at our Monetary Policy Committee meeting in July, by placing an increased emphasis on global risks, we asserted that all policy instruments might be eased should global economic problems intensify and lead to a contraction in the domestic economic activity.

Distinguished Guests,

As I stated at the beginning of my speech, global economic developments reduced risk appetite in the second quarter of the year and had an adverse impact on capital flows to emerging market economies, including Turkey. Therefore, we decreased the daily amount to be purchased via foreign exchange buying auctions in May and June. Eventually, at the beginning of this week, we suspended the foreign exchange buying auctions for some time, during which the implementation of the EU’s recent decisions and their reflections on the markets will be monitored. With another decision of the same date, we reduced foreign exchange required reserve ratios for long-term liabilities in order to encourage maturity extension of the banking sector liabilities.

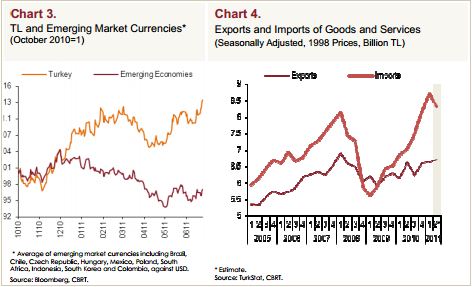

As you will recall, we underlined on several occasions that coordination among institutions is crucial for the success of the policies designed to restrain macro financial risks. In this respect, I am glad to announce that the measures taken by the Banking Regulation and Supervision Agency (BRSA) as well as the tight stance of fiscal policy have supported our policy mix implementation, and contributed to the rebalancing of domestic and external demand. As an end result of our policy implementation, the Turkish lira has continued to diverge favorably from the currencies of peer emerging markets (Chart 3). This development, coupled with the coordinated measures adopted by other institutions, has contributed to the rebalancing of domestic and external demand. In fact, leading indicators for the second-quarter suggest that the upsurge in imports has stopped while exports continue to grow in real terms (Chart 4).

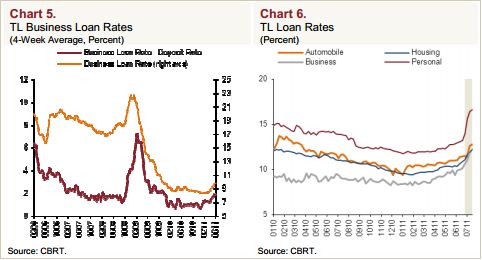

We observed that credit conditions continued to tighten in the second quarter due to measures taken by our Bank and the BRSA (Chart 5). Even though the credit growth rate has yet to decline to levels compatible with financial stability, we expect loan utilization to decelerate further in the second half of the year owing to the lagged impacts of the tightening policies. In fact, as illustrated on the slide, we see a significant rise on consumer loan rates recently (Chart 6). Accordingly, we expect that the impact of the policy mix will be increasingly more evident in the second half of the year.

2. Inflation and Monetary Policy Outlook

Distinguished Members of the Press,

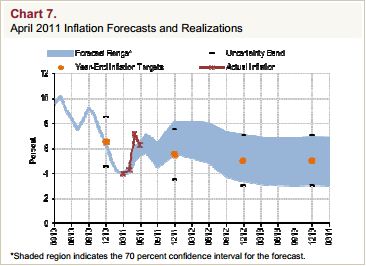

I would now like to mention the macroeconomic outlook and assumptions underlying our forecasts. First, I would like to summarize the recent inflation developments and then I will compare our short-term forecasts with data realizations in the second quarter. As you know, annual inflation, following a volatile course in the second quarter, increased to 6.24 percent. We may attribute this increase mainly to the lagged impact of import prices, rising food prices, and base effects. Although monthly inflation displayed a more volatile path than expected due to excessive volatility in unprocessed food prices, endquarter realization as of June is very close to the envisioned path presented in the April Inflation Report (Chart 7). In other words, there has been no development necessitating a revision of the initial point of our forecasts.

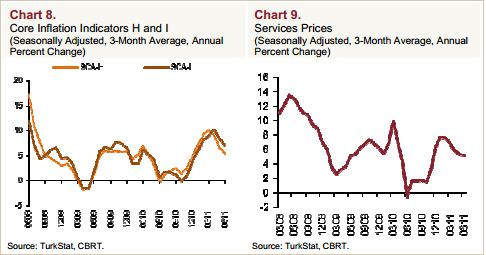

The impact of increases in commodity prices and the depreciation of the Turkish lira on inflation have continued; yet, the second round effects have been contained at this stage. At this point, I would like to emphasize that despite an increase in the annual rate of change in core indices, the seasonally adjusted monthly inflation data point to a recently declining trend (Chart 8). Moreover, we observe that the recent course of services inflation also hovers at low levels (Chart 9).

Distinguished Guests,

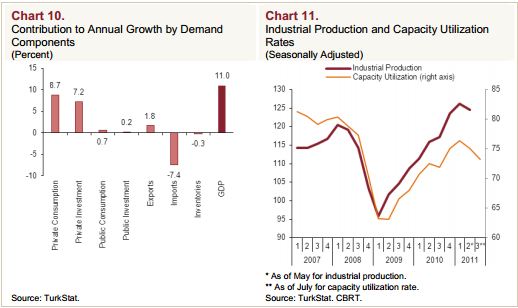

Economic activity in the first quarter of 2011 remained strong, albeit growing at a slower pace than the previous quarter. I would like to underline that this development is fully in line with the outlook presented in the April Inflation Report. The main driver of growth in the first quarter was private domestic demand (Chart 10). The divergence between domestic and external demand growth continued during this period, vindicating our new policy mix implementation.

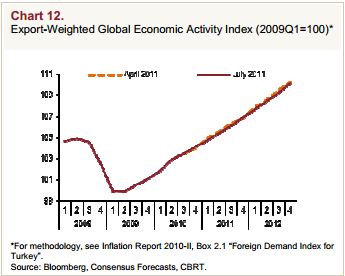

In the second quarter of the year, economic activity slowed down due to lagged impact of the tightening policies and the weak external demand. During this period, industrial production and the capacity utilization rates declined quarteron-quarter after a long time (Chart 11). We had already foreseen a slowdown in the economic activity; however, the data realizations turned out to be somewhat weaker than we expected. Therefore, our second-quarter output gap estimates were revised slightly downwards. Although downside risks have increased, downward revisions to global growth forecasts remained limited at this stage. Accordingly, outlook for Turkey's export-weighted growth index, which we use as an indicator for external demand conditions, remained broadly unchanged (Chart 12). Therefore, despite our downward revision of the output gap in the short-term, assumptions regarding external demand conditions were not subject to any major revision that might affect our inflation forecasts.

While formulating our forecasts, assumptions about oil prices for 2011 and onwards were kept at 115 USD, and there has been no significant revision for import price projections, which are calculated using future commodity prices (Chart 13). Moreover, despite the volatility in unprocessed food prices, the assumption for food inflation was maintained at 7.5 percent for end-2011 and, thereafter, as end-quarter food price realizations were very close to our projections.

On the fiscal policy side, we assumed that the extra revenues incurred via the law on restructuring of public claims would mainly be used to reduce public debt; hence, fiscal policy would tighten. Our forecasts were based on the assumption that the ratio of primary expenditures to GDP would decline slightly, the debt-to-GDP ratio would continue to fall, and the risk premium would remain broadly unchanged over the forecast horizon. Furthermore, we assumed that tax adjustments would be consistent with inflation targets and automatic pricing mechanisms.

Distinguished Members of the Press,

I would like to emphasize once more that the sustainability of the slowdown that we have observed in the pace of credit growth is crucial not only for containing inflationary pressures through controlling domestic demand, but also for macroprudential purposes through the prevention of overborrowing in the economy. Besides, in an environment where multiple policy tools are utilized, credit growth deserves particular emphasis in terms of communication of the monetary and financial conditions, as credit growth provides us with significant information regarding the evaluation of the net impact of the policy mix. Therefore, we publicly share our assumptions for the annual rate of credit growth underlying the inflation forecast in this Report as well.

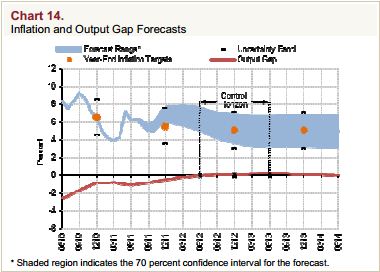

Against this background, I would like to present our inflation and output gap forecasts now. Assuming that the annual rate of credit growth declines to 25 percent at the end of the year, and the policy rate remains constant until the end of 2011, we expect inflation to be, with 70 percent probability between 5.9 and 7.9 percent with a mid-point of 6.9 percent at the end of 2011. In other words, the mid-point of our year-end inflation forecasts remains unchanged. Meanwhile, we expect inflation realizations to be between 3.5 and 6.9 percent with a mid-point of 5.2 percent at the end of 2012. Inflation is expected to stabilize around 5 percent in the medium term (Chart 14). As illustrated with the red line on the slide, our forecasts are based on an outlook where the output gap will be closed by mid-2012.

In sum, the inflation forecast path remains broadly unchanged, since there has been no significant revision to our underlying assumptions compared to the April Inflation Report.

Over the second half of the year, we project that inflation will display significant fluctuations mainly due to base effects driven by food prices. We expect that annual food inflation will decline in the third quarter, and increase in the last quarter. As shown on the slide, these fluctuations will be influential on the course of annual inflation (Chart 14).

As you may notice, our inflation forecast for the year-end is above the target of 5.5 percent. This is mainly attributable to ongoing hikes in imports prices since end-2010. So long as the second round effects remained limited, we, as the Central Bank, preferred to allow for relative external price movements balancing internal and external demand, since we consider the effect of import price developments on inflation to be one-time, as long as aggregate demand conditions remain weak – which in fact remain to be weak. Therefore, in the short term, we project a slightly above-target realization for inflation whereas in the medium term, we expect inflation to be close to the target. At this point, I would like to reiterate once more that any new data or information regarding the inflation outlook may lead to a change in our monetary policy stance. Therefore, assumptions regarding the monetary policy outlook underlying the inflation forecast should not be perceived as a commitment on behalf of the CBRT.

3. Risks and Monetary Policy

Distinguished Members of the Press,

In the last part of my speech, I would like to mention risks regarding the inflation outlook and financial stability as well as prospective monetary policy strategies to be implemented should these risks materialize.

Let me begin by saying once again that in assessing risk factors and the related monetary policy measures under current circumstances, we adopt a framework where both price stability and financial stability are taken into account. Hence, we assess risk factors not only with respect to their impact on the level, but also on the composition of the aggregate demand since the level of the aggregate demand is related to price stability, while its composition is directly related to financial stability. Hence, risk factors regarding the global economy that I will mention shortly should be evaluated also against this backdrop.

As you may recall, in building our inflation forecasts that I have just presented, we assumed in our baseline scenario that the second-quarter slowdown in the global economy will be temporary given the international institutions forecasts. Nevertheless, I would like to remind you that the developments since the April Inflation Report have increased the downside risks regarding the global economy. In other words, distribution of risk factors has changed remarkably even though the baseline scenario remained broadly unchanged. Hence, we voice the downside risks regarding the global economic activity even louder now.

Problems in credit, real estate and labor markets in advanced economies are yet to be fully solved. Moreover, concerns about fiscal dynamics in these economies still persist. Especially, mounting problems regarding the sovereign debt of euro area peripheral economies have intensified the downside risks on the global economy. We have already indicated that the interest rate corridor might be narrowed gradually, should sovereign debt problems regarding some European economies and concerns regarding global growth continue to have an adverse impact on the risk appetite. Moreover, I would like to highlight that all policy instruments may be eased, should global economic problems intensify and lead to a contraction in the domestic economic activity.

The debt problems in the euro area may certainly be resolved before they turn into a global crisis. However, even in that case, the economic activity in advanced economies may remain weak for a long period. In contrast, emerging economies may experience continuing economic growth driven by domestic demand and resurge in short-term speculative capital flows. This would mean that we may have to go through an extended period of global imbalances. This would also mean weak external demand, elevated commodity prices and rising capital flows, all feeding into macro financial risks for the domestic economy. In such a case, we may have to continue with low policy rates and high reserve requirements for an extended period in order contain risks to price stability and financial stability.

Developments in exchange rates and import prices have started to be influential on core inflation indicators since the last quarter of 2010. The hike in tariffs on fabric and apparel is another factor that may lift up core inflation indicators in the upcoming period. Under current circumstances, the increase in core inflation is a reflection of the relative price movements resulting mainly from the increases in import prices. Meanwhile, the current aggregate demand conditions contain the second round effects of the relative price movements. However, core inflation is expected to increase further in the forthcoming period, posing upside risks to inflation expectations and price setting behavior. We will not hesitate to tighten monetary policy should such a risk materialize and hamper attainment of the medium-term inflation targets. The exact mix we will use for policy tightening in such a case will depend on developments regarding domestic demand, capital flows, current account and credit growth.

We expect that the impact of the ongoing tightening measures on credit volume and domestic demand to be more significant during the second half of the year. However, I would like emphasize at this point that the extent and the timing of the impact may vary depending on developments beyond the control of the monetary policy. I would like to reiterate that we will continue to closely monitor the lagged effects of the adopted policy measures on price and financial stability, and take additional measures if deemed necessary.

We will continue to monitor fiscal policy developments closely while formulating monetary policy. Sustaining the fiscal discipline under current circumstances remains essential to limit risks posed by the current account deficit driven by the divergence between domestic and external demand. Saving the extra revenues acquired via the restructuring of public claims and strong economic activity would not only reduce risks to price stability and financial stability, but also enhance the effectiveness of the new policy mix. In this respect, we assumed in building our baseline scenario forecasts that the extra budget revenues will be saved to a large extent. We may have to revise the monetary policy stance should the fiscal stance deviate significantly from this framework, and, consequently, have an adverse effect on the medium-term inflation outlook.

In the period ahead, we will continue to focus on building price stability on a permanent basis while observing financial stability as a supportive objective. To this end, we will also carefully assess the impact of the macroprudential measures taken by our Bank and other institutions on the inflation outlook. Strengthening the commitment to fiscal discipline and the structural reform agenda in the medium term would support the relative improvement of our sovereign risk, and thus facilitate macroeconomic and price stability. Sustaining the fiscal discipline will also provide room for monetary policy maneuver, and support social welfare by keeping interest rates permanently at low levels. In this respect, I would like to remind you once more that the timely implementation of structural reforms envisaged by the Medium Term Program and the European Union acquis communautaire remains to be of utmost importance.

Thank you very much for your participation.