Governor Başçı's Speech in Press Conference for the Presentation of the Inflation Report-I (Ankara, 29/01/2013)

Distinguished Guests,

Welcome to the press conference held to convey the main messages of the first Inflation Report of the year. Today I will talk about recent global and domestic developments besides the CBRT’s inflation forecasts that are accordingly updated. I will now present an overview of the report, which will be published on our web-site shortly.

The Report typically summarizes the economic outlook underlying monetary policy decisions, shares our evaluations on macroeconomic developments and presents our medium-term inflation forecasts which were revised in view of the developments in the last quarter, along with our monetary policy stance. In addition to the main text, the Report includes nine boxes entailing significant and up-to-date analyses on various topics. For instance, one of these boxes presents an analysis on the level of credit growth rate which will prove reasonable and healthy for Turkey in the period ahead. Moreover, there is a summary of two papers examining the effects of the CBRT’s latest policies on the expectations and volatility of the foreign exchange rate. In the Report, there are also analyses on the current account balance, global risks, accounting of inflation forecasts, tax adjustments on the tobacco products and the sensitivity of tax revenues on the economic circumstances. Titles of the boxes are shown on the slide. I strongly recommend that you read these boxes, which will be published on our web-site shortly.

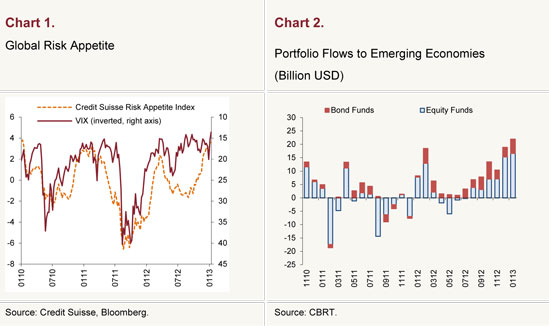

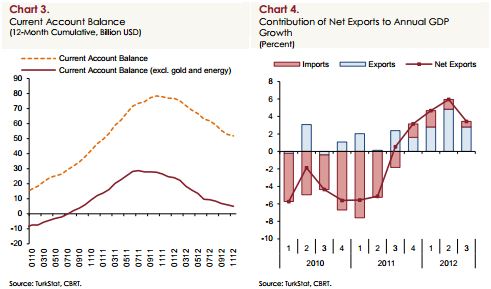

Now, I would like to convey the main messages of the report. Firstly, I will touch upon the global economy and then move on to the monetary policy. The last quarter of 2012 was marked by an improvement in the risk appetite (Chart 1). Concrete steps taken towards the resolution of the Euro area problems as well as the favorable news regarding the US and Chinese economies were the leading developments that fed into the risk sentiment. On the other hand, quantitative easing policies were sustained amid the persisting sluggish growth outlook in advanced economies. Continued monetary easing at a global scale accompanied by increased risk appetite led to an acceleration in portfolio flows towards emerging economies (Chart 2). We are of the opinion 3 that all these developments once again highlighted the importance of a flexible monetary policy framework.

1. Monetary Policy and Monetary Conditions

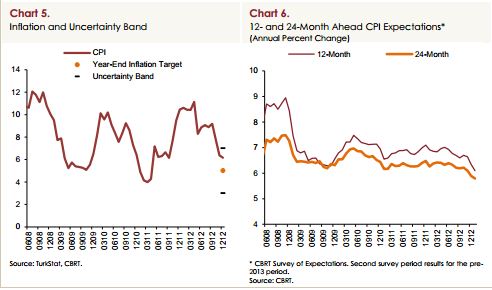

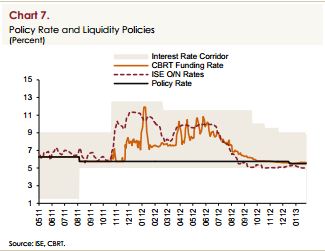

In this period of extraordinary global circumstances, the policy framework designed by the CBRT plays a great role in confining the adverse impacts of global shocks in Turkey. Particularly the year 2012 was marked by the fruitful implementation of our policy mix. Persisting global imbalances notwithstanding, we witnessed a healthier outlook composition of growth besides a more evident rebalancing process. As illustrated in the slide, the current account continued to improve (Chart 3) and the contribution of net exports to growth displayed a surge (Chart 4). I would like to put special emphasis on the contribution of both exports and imports, which proved positive, highlighting the effectiveness of the measures taken.

The year 2012 was not only a year of rebalancing but also a period of important achievements on the price stability front. Inflation trended downwards throughout the year and fell by 4.3 percentage points year-on-year. Moreover, medium-term expectations showed a remarkable improvement for the first time after a protracted period (Charts 5 and 6).

Having started to achieve the intended results regarding inflation and rebalancing, monetary policy has adopted a more accommodative stance since mid-2012. In this respect, the CBRT lowered its average funding rate gradually since June by increasing the liquidity injected to the market (Chart 7). Improved risk appetite and more effective use of the Reserve Options Mechanism (ROM) have allowed a gradual reduction in the upper bound of the interest corridor since September. Meanwhile, the liquidity provided for the market was further increased, driving overnight market rates close to lower bound of the corridor.

Capital inflows accelerated at the year-end upon the surge in global risk appetite coupled with a relative improvement in risk perceptions regarding Turkey. This contributed to a faster-than-expected credit growth and appreciation pressures on the Turkish lira. I suppose you remember that we stated this as a possible risk scenario in the previous Inflation Report and listed possible measures we could take. Upon the materialization of these risks to a large extent, we launched the strategy we envisaged. In order to contain the risks on financial stability, the appropriate policy response would be to keep interest rates at low levels while sustaining macroprudential measures. In this respect, the policy rate and the corridor have recently been shifted down and a measured tightening has been implemented through reserve requirement policy.

Despite the cut in short term interest rates, the CBRT maintained its cautious and flexible stance, which is worth noting. Thus, I would like to reiterate that the impact of the measures taken on credit, domestic demand and inflation expectations will be closely monitored and the amount of the Turkish lira funding will be adjusted in either direction, as needed.

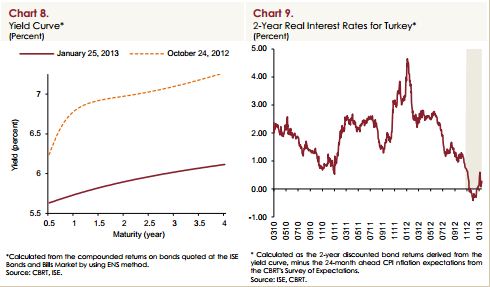

Market interest rates plummeted in the last quarter due to improved risk appetite besides the liquidity policies pursued by the CBRT. Meanwhile, the decline in long term rates proved more notable. As a consequence, yields shifted down across all maturities while the yield curve flattened in the interreporting period as illustrated in the slide (Chart 8). Real interest rates also plunged since the fall in nominal interest rates was more significant than that in inflation expectations. Although having crept up recently, real rates still stand at ever-low levels (Chart 9).

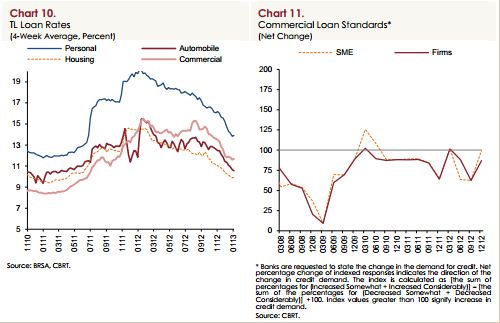

Bank lending rates also remained on a downward track in the last quarter amid eased external financing conditions alongside our liquidity policy. Consumer loan rates maintained a downward trend in line with the market interest rates. Moreover, the fall in corporate loan rates became more significant in the final quarter of the year owing to the cuts in the upper bound of the corridor (Chart 10). What is more, tightening in the credit supply conditions for corporate lending receded in this period (Chart 11).

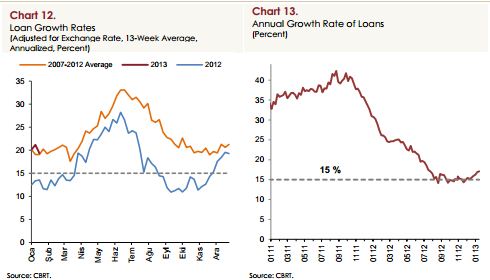

As a result of these developments, credit growth gained pace in the last quarter of the year (Chart 12). Accordingly, annual rate of growth in total credit stock materialized around 16 percent at the end of the year, slightly higher than the 15 percent benchmark level for the medium term (Chart 13). Total credit growth proved robust in early 2013, and the uptrend of 13 weeks in credit volume stood close to the past years’ average.

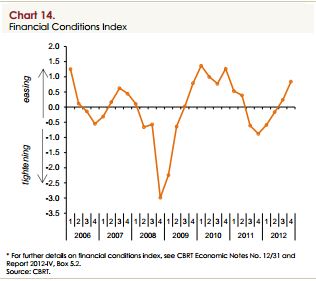

There is a risk of further acceleration in credit in the forthcoming period. Financial conditions index continued to ease with rapid capital inflows, improving credit supply conditions, and accommodative liquidity policy (Chart 14). This outlook necessitates a cautious stance against macro financial risks. Given these evaluations, I would like to remind that in its first monthly meeting of 2013, the Committee highlighted the faster-than- expected credit growth and signaled that macroprudential measures might be continued should this trend persist.

2. Macroeconomic Developments and Assumptions

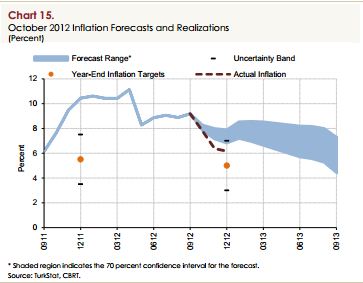

Now, I will talk about the macroeconomic outlook and our assumptions which constitute the basis for our forecasts. First, I will summarize the recent inflation developments, and then compare the short term forecasts in the October Inflation Report with the actual year-end inflation data in 2012. Then, I will continue with the domestic and foreign demand outlook. Consumer inflation undershot the forecasts in the last quarter of 2012 and stood within the uncertainty band (3-7 percent) with 6.2 percent at the year-end (Chart 15). This lower-than-envisaged inflation rate was mainly driven by the developments in unprocessed food prices, which were stated to pose downside risk on inflation in the October Inflation Report. Meanwhile, core inflation indicators were broadly consistent with expectations.

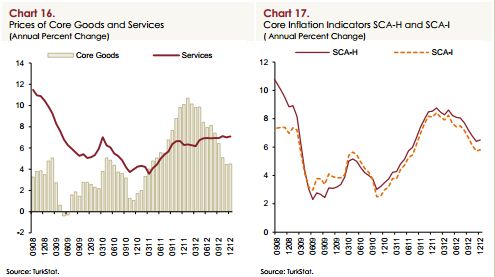

Cumulative effects of the previous year’s exchange rate and import price movements gradually waned. Coupled with the ongoing slowdown in domestic demand, this led to a sustained fall in the annual rate of increase in core goods prices. Meanwhile, prices of services remained on a mild track (Chart 16). Against this backdrop, core inflation indicators maintained a downward trend (Chart 17).

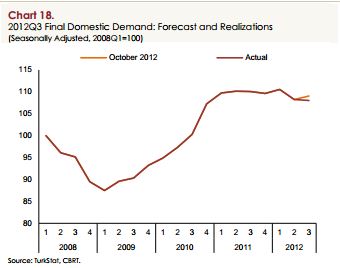

Now, I will touch upon the developments in economic activity on which the inflation forecasts are based besides the short term outlook. Third-quarter national income data point that domestic demand conditions remained weak due to private investment demand. Private consumption, which displayed an increase for the first time in a protracted period, limited the slowdown in final domestic demand. Nevertheless, demand conditions followed a slightly weaker course compared to the projections in the October Inflation Report (Chart 18). Last-quarter data indicate a mild pick-up in consumption and investment demand as envisaged. Accordingly, output gap forecasts regarding the second half of 2012 are slightly revised downwards compared to the previous report.

Meanwhile, we estimate that easing financial conditions due to the recent rise in capital inflows may result in a higher-than-expected growth in final domestic demand in the first half of 2013. Indicators for orders, loans and other leading indices also support this outlook. Accordingly, we based the projections on a stronger domestic demand outlook for the first half of 2013 compared to the previous reporting period.

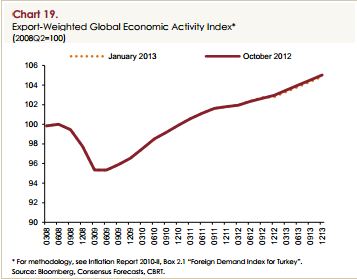

On the other hand, external demand remains subdued. This period did not see a notable change in global growth projections; hence there was no significant revision in export-weighted global growth index (Chart 19). Accordingly, our forecasts are based on an outlook that entails a mild increase in exports driven by market and product diversification as in the previous report.

In short, in line with the developments in domestic and external demand, the contribution of aggregate demand conditions to disinflation is envisaged to be larger in the second quarter of 2012; but smaller at the start of 2013 compared to the previous report. Overall, given the lagged effects on inflation, I would like to state that the revision in the output gap did not bring about a noticeable effect on the end-2013 inflation forecast.

As you all know, food, energy and import prices also play a great role in inflation forecasts. Therefore, before moving on to forecasts, I will briefly talk about our assumptions regarding these variables.

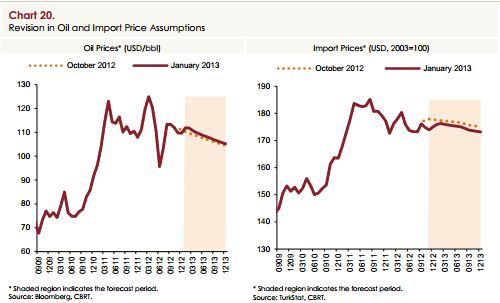

The outlook for import prices did not exhibit a notable change in the interreporting period (Chart 20). The assumption for average oil prices for 2013, which was USD 107 in the October Inflation Report, was slightly revised upwards to USD 108 in line with the futures prices. Due to the favorable course of non-energy import prices, we revised our assumption for import prices slightly downwards in the interreporting period (Chart 20). However, I would like to underline that this revision did not bring about a noticeable effect on the inflation forecast for 2013. Meanwhile, the assumption for the annual rate of increase in food prices was preserved at 7 percent as it was in the previous report. In other words, we assumed that the favorable course of unprocessed food prices in 2012 would come to a halt in the forthcoming period.

Before moving on to projections, I will dwell on our assumptions about the public finance. Developments in the fiscal policy and tax adjustments in the last three months were broadly consistent with the assumptions laid down in the October Inflation Report. Effects of the adjustments in tobacco products on inflation in January proved to be as expected. Furthermore, the year-end budget balance was consistent with the targets revised in the Medium Term Program (MTP).

Medium term projections are based on the assumption that no additional tax adjustments will be introduced to tobacco and energy products in the rest of the year. On the other hand, I would like to mention that other tax adjustments and administered prices are assumed to be consistent with inflation targets and automatic pricing mechanisms.

Regarding the fiscal outlook, medium-term inflation forecasts take the revised projections of the MTP as given. Accordingly, it is assumed that fiscal discipline will be preserved and the structural budget balance will not display a notable change in the forthcoming period. Thus, there has been no change in end-2013 inflation forecast stemming from fiscal policy.

Thus, I can say that assumptions underlying inflation forecasts and external conditions were broadly kept unchanged.

3. Inflation and Monetary Policy Outlook

Now, I would like to present our inflation and output gap forecasts based on the outlook I have described so far. I would like to remind you that medium term forecasts assume that monetary policy decisions are data dependent.

Accordingly, we envisage that credit and exchange rates follow a stable course and aggregate demand conditions are kept at levels that do not exert upside pressures on inflation. In other words, we based our forecasts on an outlook where risks arising from the recent surge in capital inflows risks are contained.

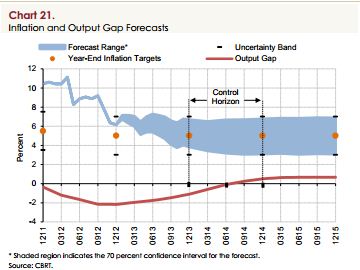

When forming our forecasts, we assumed that annual loan growth rate would hover around 15 percent and there would be no significant change in the real effective exchange rate. Accordingly, inflation is expected to be, with 70 percent probability, between 3.9 and 6.7 percent (with a mid-point of 5.3 percent) at the end of 2013, and between 3.1 and 6.7 percent (with a midpoint of 4.9 percent) at the end of 2014. We expect inflation to stabilize around 5 percent in the medium term (Chart 21).

In sum, we maintained inflation forecast for end-2013 at 5.3 percent, as there has been no major revision in the factors affecting inflation outlook in the past three months.

We expect inflation to resume its downward trend after creeping up in January due to tobacco price adjustments. Although inflation may increase temporarily in May and June due to base effects in energy prices, it will continue to decline in the following months, closing the year at 5.3 percent (Chart 21). We expect core inflation indicators to display a steady downward path and materialize below 5 percent at the end of the year.

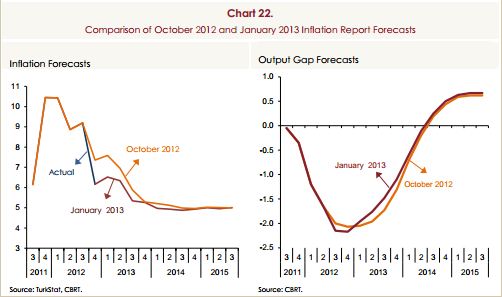

Revisions in our inflation forecasts are presented on the slide. Although there was no change in the end-year inflation forecast, we revised our inflation forecasts downwards compared to the path presented in the October Inflation Report in the short term due to the benign course of unprocessed food prices (Chart 22).

The same slide presents the revision in the output gap forecasts. We revised the output gap upwards for the first quarter of 2013 due to recent acceleration in capital inflows and credit growth. However, we assumed that the policy measures would drive the output gap and credit path closer to the October forecast in the second half of the year.

We can summarize the main message of the forecast regarding the monetary policy as follows: a cautious monetary policy stance should be maintained to keep inflation close to the target at the end of 2013. It is important that the CBRT does not disregard excessive volatility in credit and exchange rates, for macro financial risks to be contained. It should be kept in mind that keeping credit growth at healthy and reasonable levels will support both price stability and financial stability. In fact, notwithstanding the recent faster-than-expected growth in credit, we envisaged that credit growth would hover around 15 percent.

I would like to once more underline that any new data or information regarding the inflation outlook may lead to a change in the monetary policy stance. Therefore, assumptions regarding the monetary policy outlook underlying our inflation forecasts should not be perceived as a commitment on behalf of the CBRT.

In addition to these forecasts, alternative scenarios on the inflation outlook and the global economy are discussed in the Risks section of the Inflation Report. You can examine the Report for details.

While concluding my remarks, I would like to thank all my colleagues, who contributed to the Report, primarily those at the Research and Monetary Policy Department as well as the members of the Monetary Policy Committee, and thank every one of you for your participation.