Changes in international crude oil prices impact domestic fuel prices, which in turn affect the inflation outlook. The sliding scale system, implemented to mitigate the effects of rising global oil prices on consumer prices, functions as an automatic stabilizer. The system is designed to limit the impact of rising oil prices on fuel prices through adjustments to tax components. In this blog post, we explore the potential impact of the sliding scale system, initiated in March 2026, on inflation dynamics.

For 2026, fuel expenditures have a share of 3.21% in the consumer basket. The increase in fuel prices directly affects consumer inflation through this channel, and indirectly affects many sectors, particularly transport services and unprocessed food, through the cost channel. Additionally, sudden changes in fuel prices, which garner significant public attention, play a crucial role in shaping expectations and influencing price-setting behavior. Therefore, fluctuations in fuel prices are important for both the short-term trajectory of inflation and the price pressures arising from cost and expectation channels.

How does the sliding scale mechanism work?

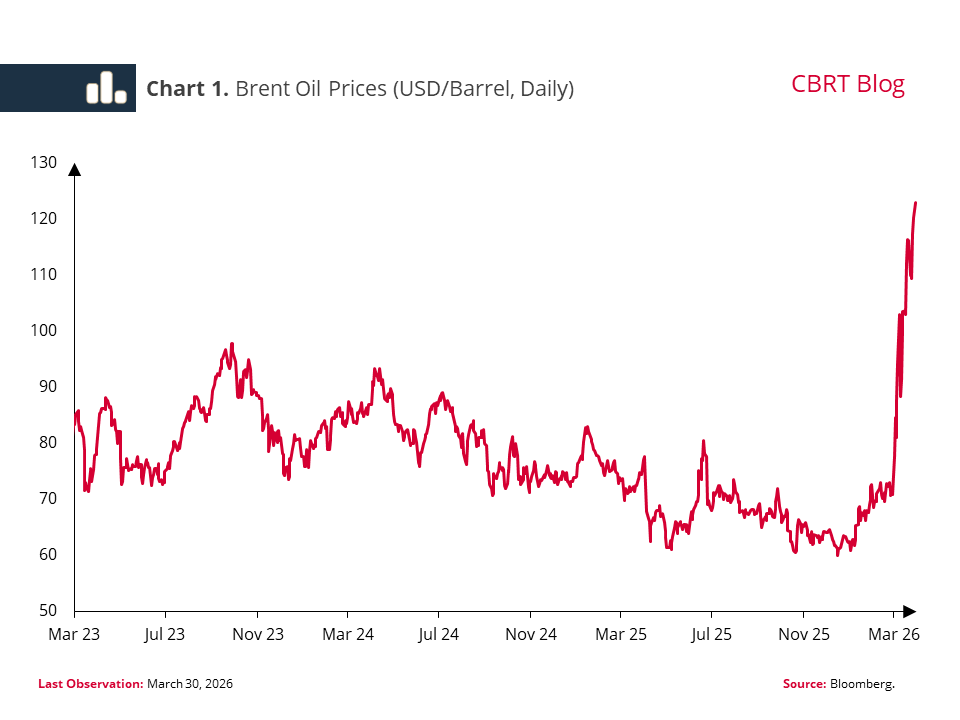

Fuel prices are the sum of product prices, refinery-distributor-retailer margins, income share of the Energy Market Regulatory Authority (EMRA), and sum of total taxes. The key determinants of product prices are international oil prices, refinery margins and exchange rates. Amid the recent geopolitical unrest, international oil prices have risen sharply (Chart 1). That’s where the sliding scale system kicked in upon the Presidential Decision of March 4, 2026, along with adjustments made to the portions of the Special Consumption Tax (SCT) imposed on fuel products.[1]

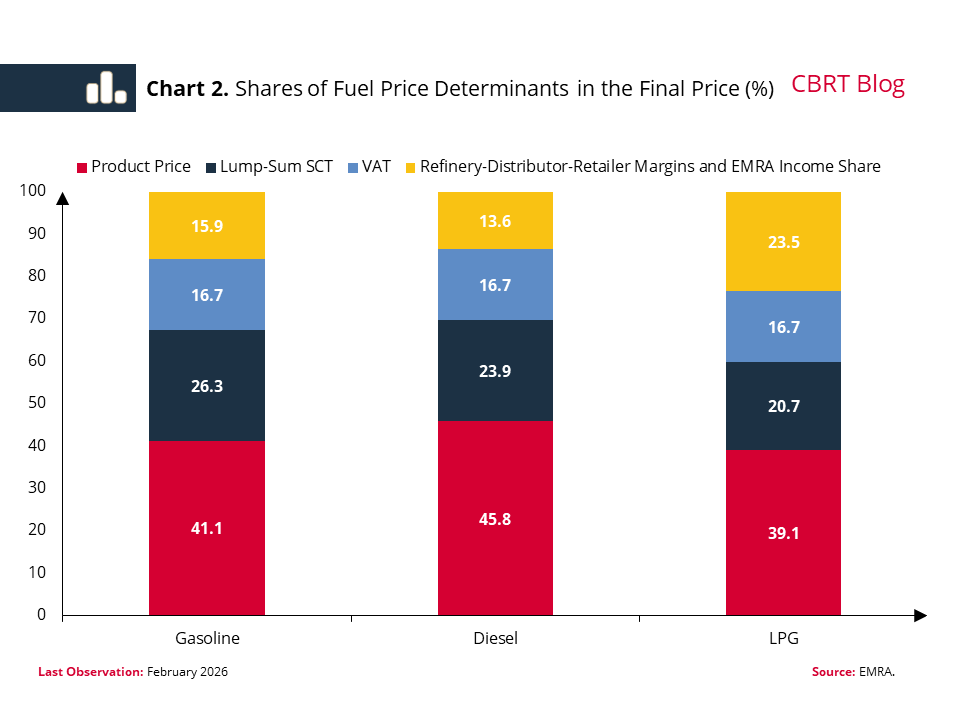

The sliding scale system functions as a mechanism that partly offsets the impact of changing costs on fuel prices through tax adjustments, thereby easing price volatility. At times of elevated prices in gasoline, diesel or LPG products, this mechanism is used to reduce the tax component, hence to limit the increase in final fuel prices. The fact that fuel prices are the sum of different components allows the mechanism to function through the tax item.[2] In fact, as of February 2026, the approximate shares of lump-sum SCT amounts were 26% for gasoline, 24% for diesel, and 21% for the LPG (Chart 2).

How much of a restraining effect will the current sliding scale system have on headline inflation?

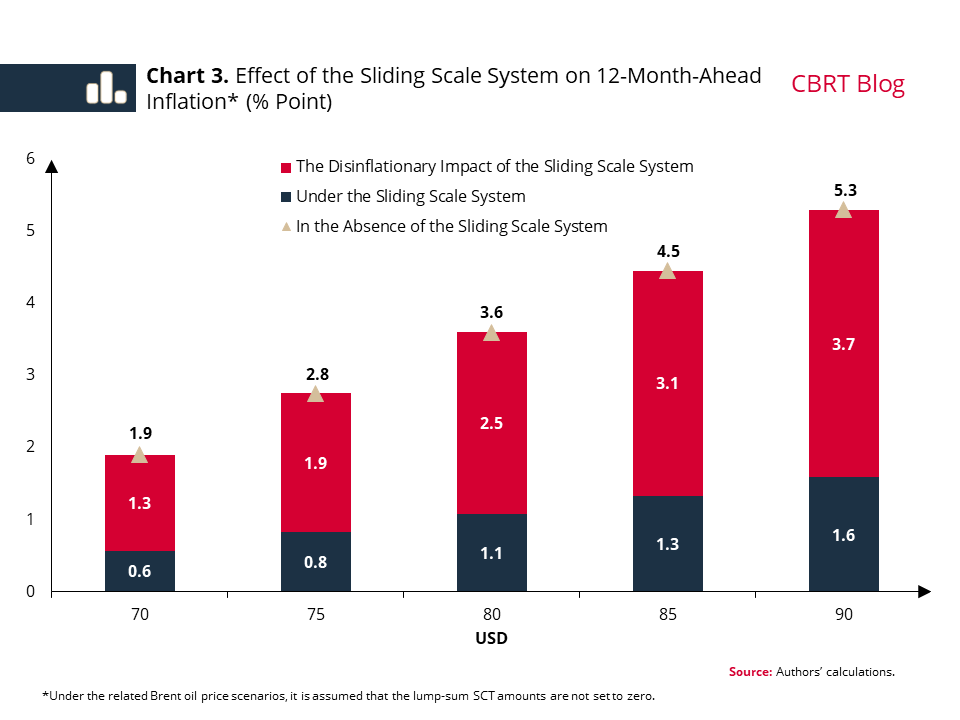

To gauge this effect, we need three key parameters. The first one is the trajectory of global oil prices. The second parameter is the degree of the impact of global oil price changes on product prices (cited under the CIF MED heading in the Platts European Market Scan) that Türkiye has set as a benchmark for fuel price formation. Here, we assume a one-to-one pass-through from Brent oil prices to product prices. The third parameter is the coefficient of the pass-through from the Brent oil price increase to headline inflation in the absence of the sliding scale system. To calculate this coefficient, we revise the work published in 2025 so as to include the recent period.[3] Our findings suggest that a 10% rise in the Brent oil price ultimately increases consumer inflation by 1 percentage point over the next 12 months, operating through both direct and indirect effects. We calculate the total effect over the next 24 months at approximately 1.2 percentage points.

In the first Inflation Report of 2026, the Brent oil price assumption averaged USD 58.8 between March 2026 and February 2027. In our analysis, we explore alternative scenarios in which the average Brent oil price varies from USD 70 to USD 90 over the next 12 months (March 2026-February 2027) (Chart 3). Under the scenario where the average Brent oil price is USD 70, the pass-through from Brent oil to product prices is one-to-one and the sliding scale system is not in use, the upward effect on the annual inflation forecast is 1.9 percentage points at the end of the 12-month period. The sliding scale system allows the direct and indirect increases in inflation to be 1.3 percentage points lower, corresponding to 0.6%. With an average Brent oil price of USD 90, the sliding scale system would lower the effect on annual inflation by up to 3.7 percentage points.

In summary, the sliding scale mechanism can significantly mitigate inflationary spillovers resulting from rising international energy prices driven by geopolitical developments, and unaffected by monetary policy. We believe this arrangement will support the disinflation process.