Cyclical effects, which are temporary effects such as fluctuations in foreign trade prices and economic activity, may overshadow the structural part of the current account balance that incorporates relatively long-term trends. Therefore, to make more accurate inferences and assessments pertaining to the current account balance, it is important to adjust the headline current account balance for cyclical effects and monitor structural changes. When cyclical effects are taken out, we calculate that the Turkish economy posted a current account surplus for the first time in the analyzed period and for the last three quarters in a row.

The cyclically-adjusted current account balance provides clues pertaining to the outlook of current account balance that would prevail under the assumption that long-term trends and foreign trade prices were maintained in domestic and international economic activity. Taking into account the fact that the impact of each cyclical effect on each variable may vary, we created output and price gap series by detecting the long-term trends of price and demand variables separately with the help of the Fully Modified Hodrick-Prescott (FMHP) filter [1] . While making calculations, we assumed that the long-term stable relationship between the import amount excluding gold and real domestic demand, and the real export amount excluding gold and foreign demand were preserved [2].

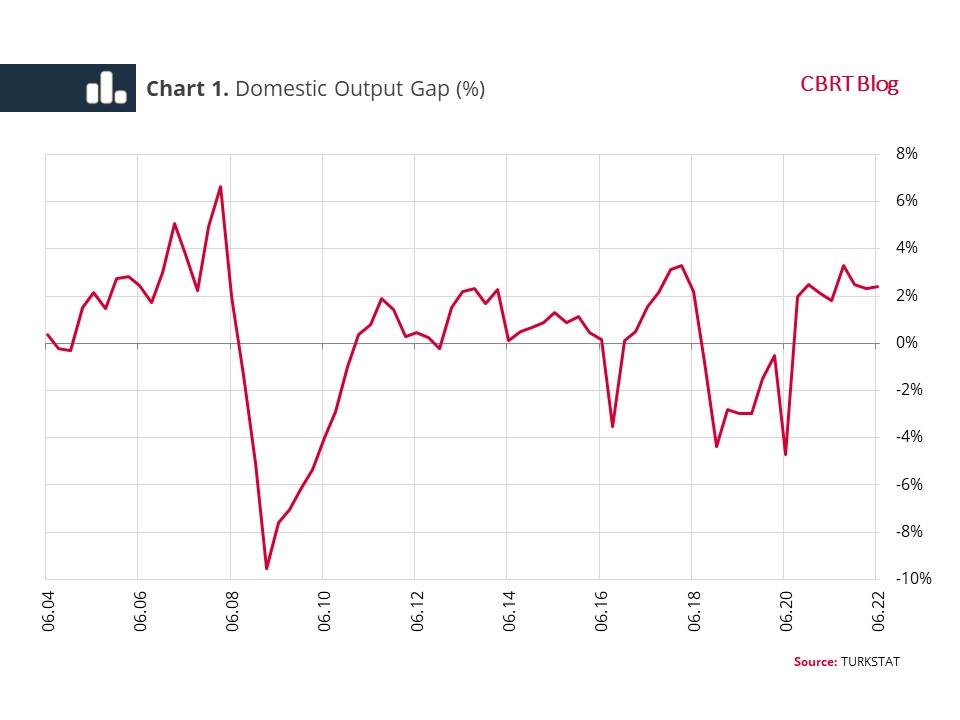

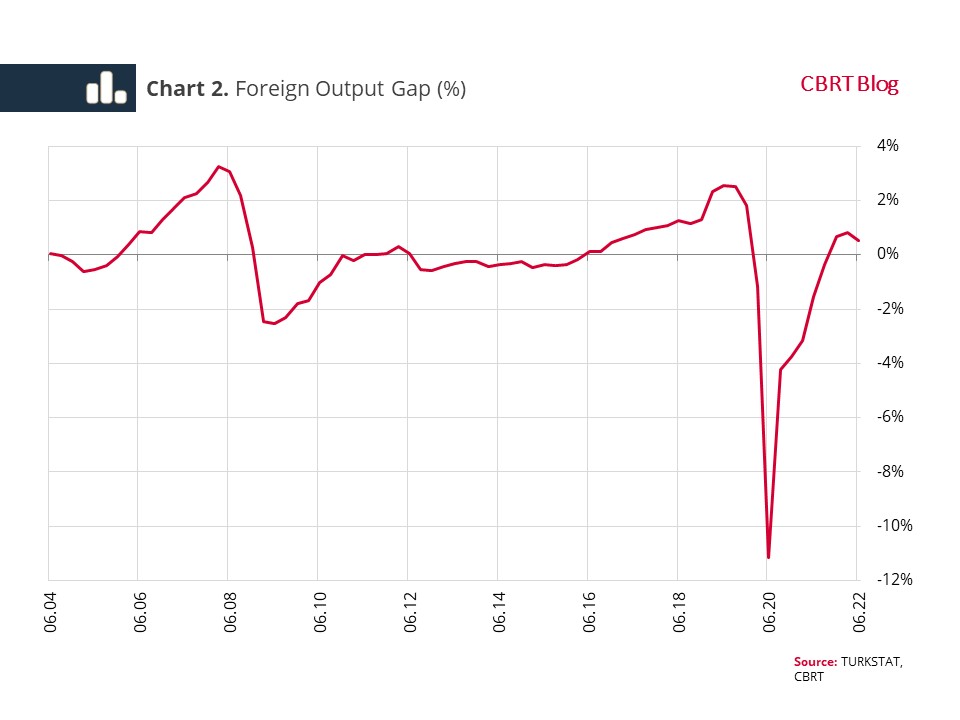

Real Gross Domestic Product (GDP) was used as the domestic demand variable and the Export-Weighted Global Growth (EWGG) [3] index was used for the foreign demand variable, and long-term trends were estimated by employing the FMHP filter to reach the output gap series (Chart 1 and Chart 2). We observed that the domestic output gap remained in the negative territory from the second half of 2018 till the second half of 2020, then turned positive and remained in the positive territory in the following period. The foreign demand or output gap, which went into the negative territory due to the coronavirus pandemic, turned positive in the last quarter of 2021. Meanwhile, in the post-pandemic period, foreign demand mostly remained below its long-term trend, and export demand reclaimed its long-term trend as late as the end of 2021.

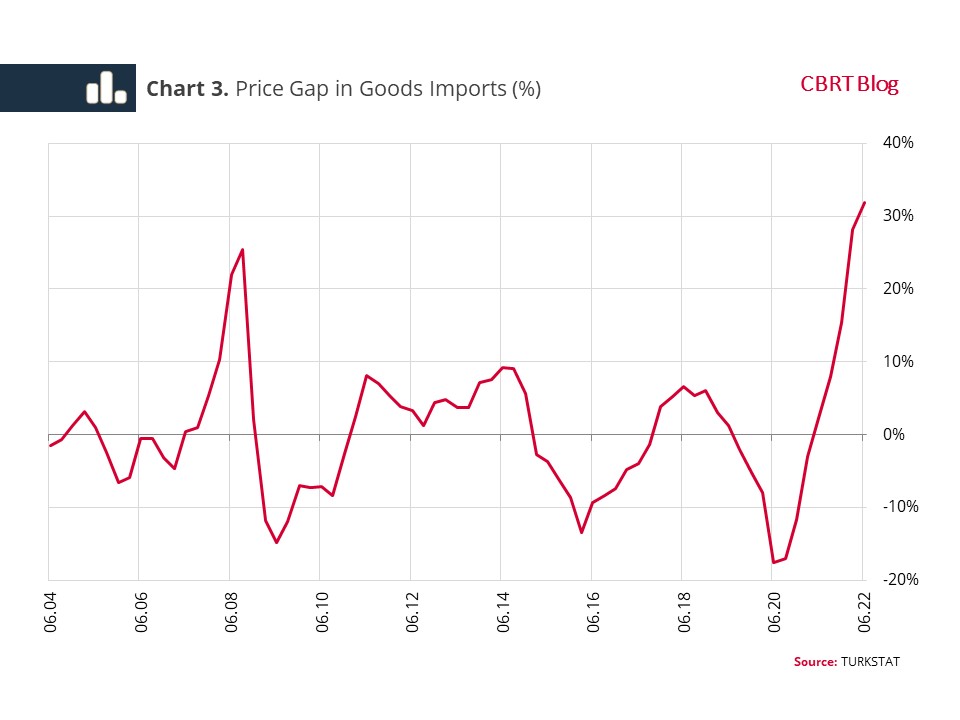

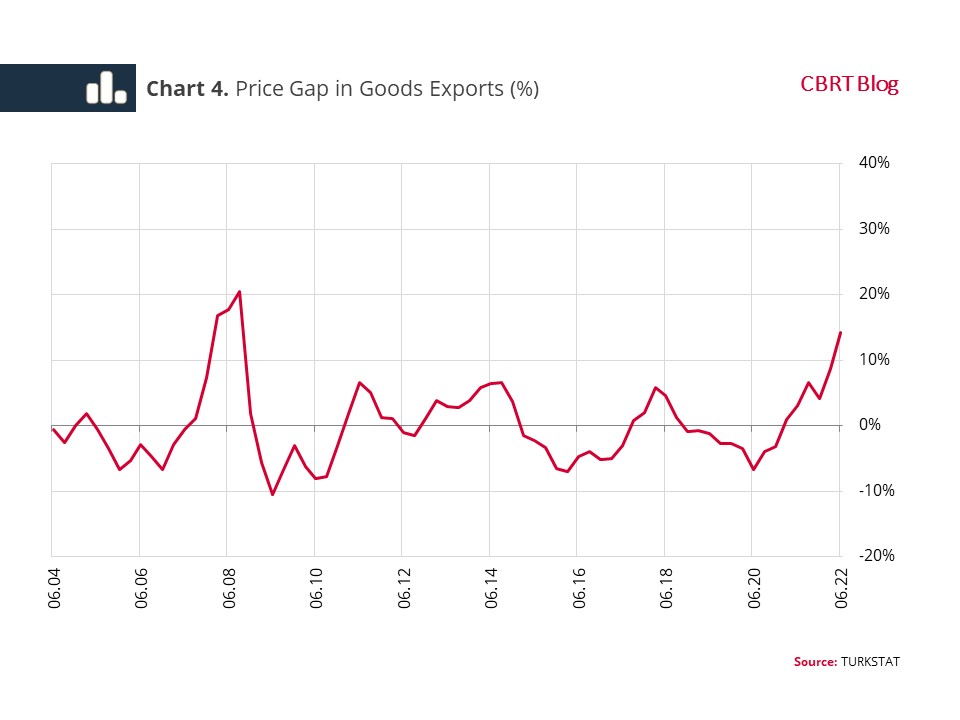

We obtained price gap series for Turkey's export and import prices by using the FMHP filter. For information purposes on the outlook of price series, Charts 3 and 4 present price gap series calculated for imports and exports of goods. During the pandemic, both export and import prices rapidly fell below their long-term trends but rose above the trends in the post-pandemic period. Despite a partial improvement in supply constraints in the post-pandemic period, supply fell short of meeting the increasing demand, and thus, the world prices of commodities, of which Turkey is a net importer, increased. The Russia-Ukraine conflict that broke out at the beginning of 2022 also played an important role in the rise in agricultural and energy commodity prices. In this context, it is noteworthy that in the last quarter of 2021 and the first quarter of 2022, the import price gap was significantly more positive than the export price gap. This situation fueled the increase in foreign trade and therefore the current account deficit.

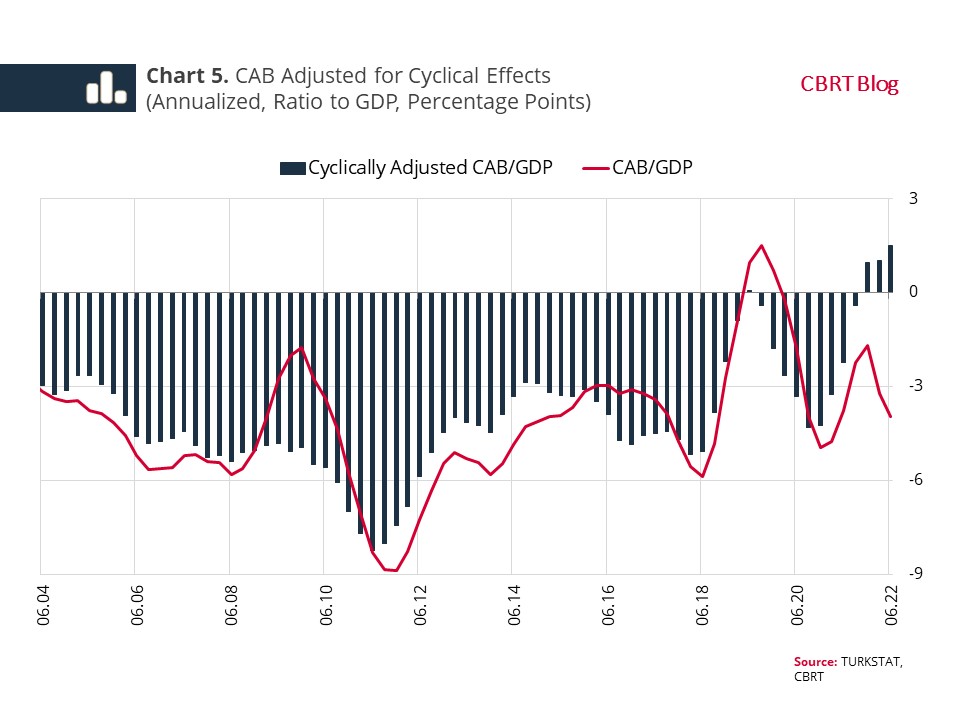

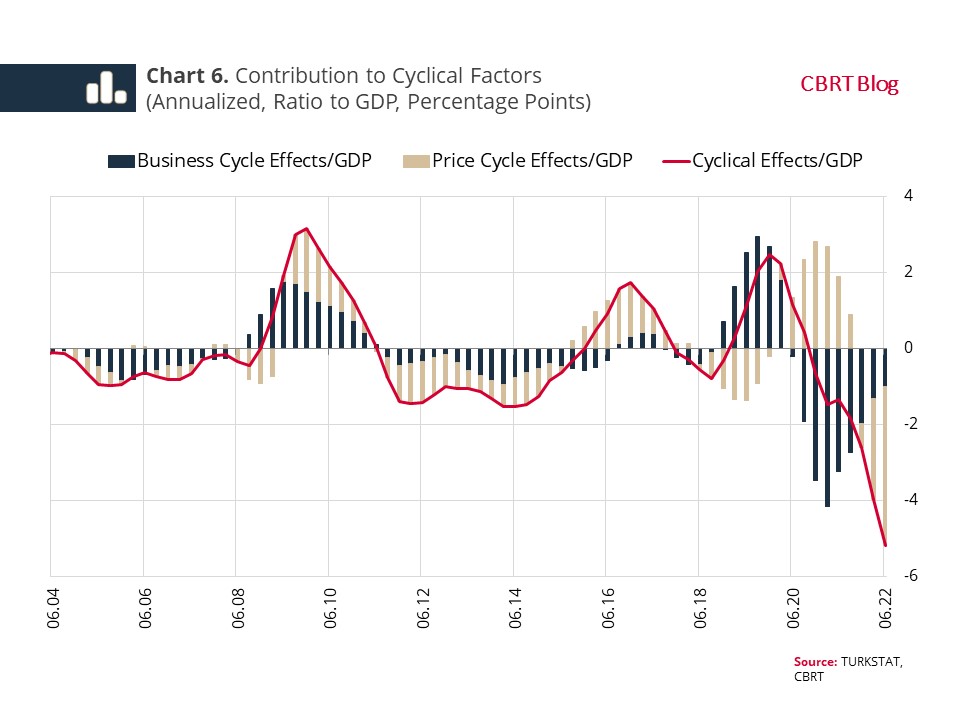

Chart 5 shows the cyclically-adjusted current account balance that mostly contains structural elements. In the last quarter of 2021, the cyclically-adjusted CAB rose significantly above zero for the first time historically (2003-2021), and this was maintained in the first two quarters of 2022. The effect of business cycles turned negative as of the second quarter of 2020 and decreased (increased) the current account balance (deficit) in the following periods (Chart 6). Particularly, in the first quarter of 2020, prices decreased significantly due to the decrease in global demand because of the pandemic, and the effect of the price cycle had an increasing (lowering) effect on the current account balance (deficit) until the last quarter of 2021. In the final quarter of 2021 and in the first two quarters of 2022, the effect of the price cycle turned significantly negative, as import prices rose faster than export prices led by the rise in global commodity prices. The recent foreign trade shock has increased the headline current account deficit, nevertheless, the cyclically adjusted current account balance is running a surplus, pointing to an improvement driven by more structural factors.

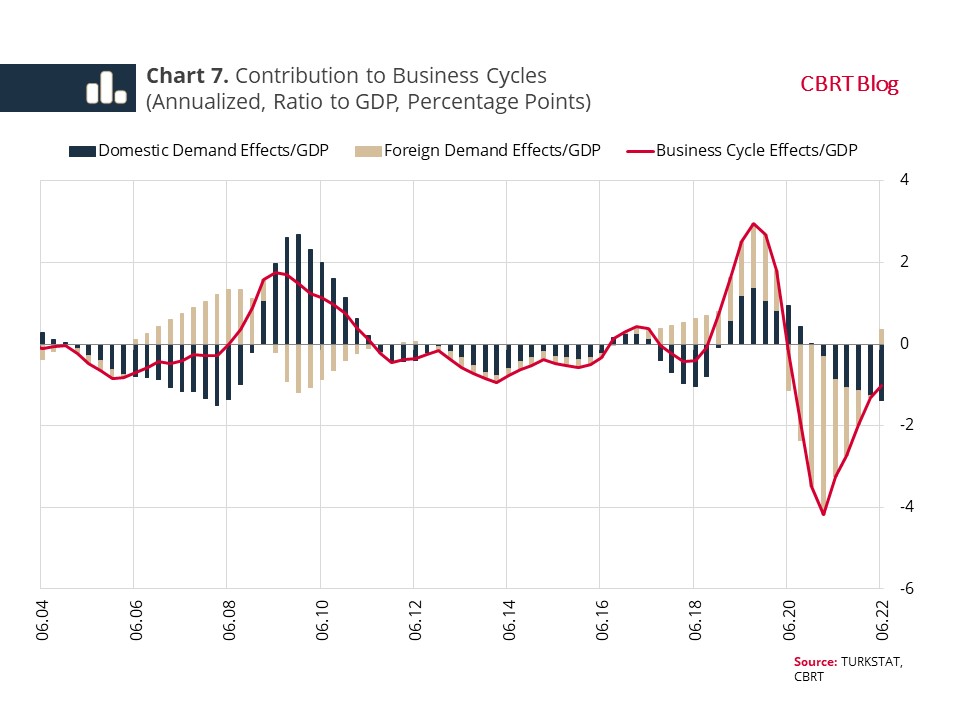

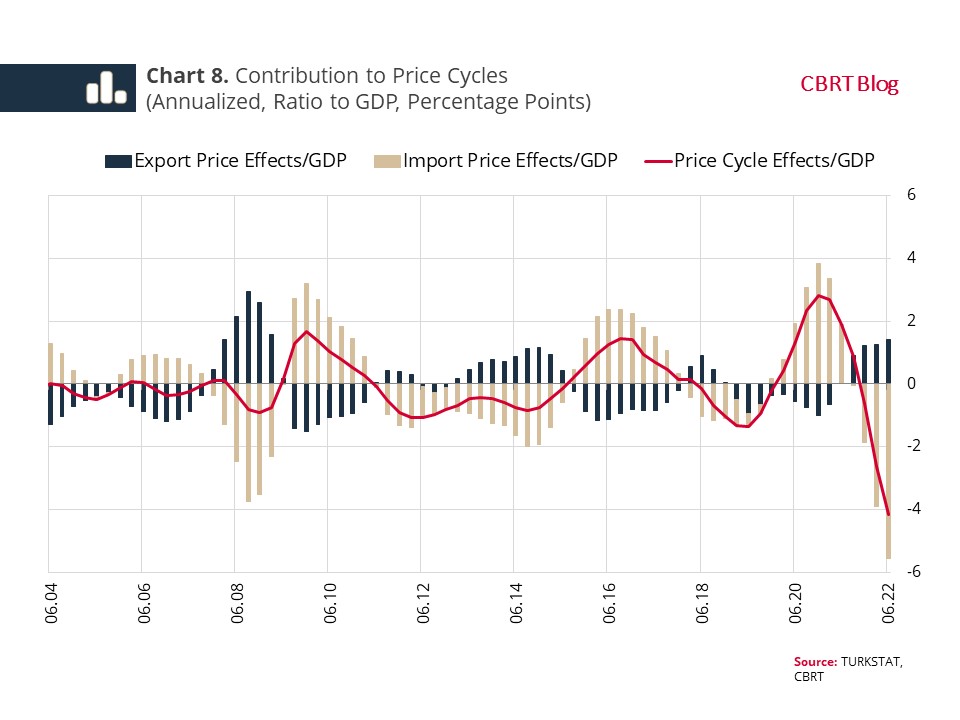

As the domestic GDP fell below its long-term trend during the pandemic, the domestic business cycle effect was positive, while the international business cycle effect was negative because the foreign demand fell below its long-term trend (Chart 7). In this period, the overall business cycle effect was negative, as the foreign business cycle effect was stronger. On the back of the rapid recovery in domestic demand in the post-pandemic period, the domestic business cycle effect was negative, while the foreign demand recovered gradually and the foreign business cycle effect remained in the negative territory. Import prices remained below their long-term trend during and after the pandemic and while the import price cycle effect pushed current account balance up export prices remained below their long-term trend, and the effect of export price cycles had a downward impact on the current account balance (Chart 8). The price cycle effect, which was positive during and after the pandemic, increased the current account deficit significantly as the import price cycle turned negative rapidly and strongly in the final quarter of 2021, and the negative effect grew in the following two quarters.

To sum up, recently, domestic and international business cycles and import price cycles have made a decreasing (increasing) impact on the current account balance (deficit). On the other hand, the cyclically-adjusted current account balance, which includes more structural elements, continued to improve and posted a positive value for the first time at the end of 2021, and maintained this outlook in the first two quarters of 2022. If the cyclical effects ease and particularly, if global commodity prices converge to their long-term trends, the deficit observed in the headline current account balance may decrease significantly and even post a surplus.

[1] For details of the FMHP filter, please see Hanif et al. (2017).

[2] The method for adjusting for cyclical effects is explained in detail in Eren and Tuzun (2019).

[3] For calculation method and more details of the EWGG, please see Eren and Yavuz (2020).

References

Eren, O. and Tüzün, G. (2019), “Cyclically Adjusted Current Account Balance of Turkey”, CBRT Working Paper, No.19/34.

Eren, O. and Yavuz, D. (2020), “Export-Weighted Growth Indices by Regions”, CBRT Research Notes on Economics, No.20/02.

Hanif, M. N., Javed I., and Choudhary, M. A. (2017), "Fully Modified HP Filter," SBP Working Paper Series No.88.