The recent rise in the foreign currency (FX) deposits[1] has sparked interest in the developments in demand for Turkish lira (TRY). In this blog post, we analyze the relation between the growth in FX deposits and the reduction in the FX-protected deposit (KKM) balances in light of data, and interpret this relationship in the context of savers’ currency preferences. Our analysis suggests that the rise in FX deposits aligns well with the accelerated decline in KKM balances and that the preference for Turkish lira savings continues to grow.

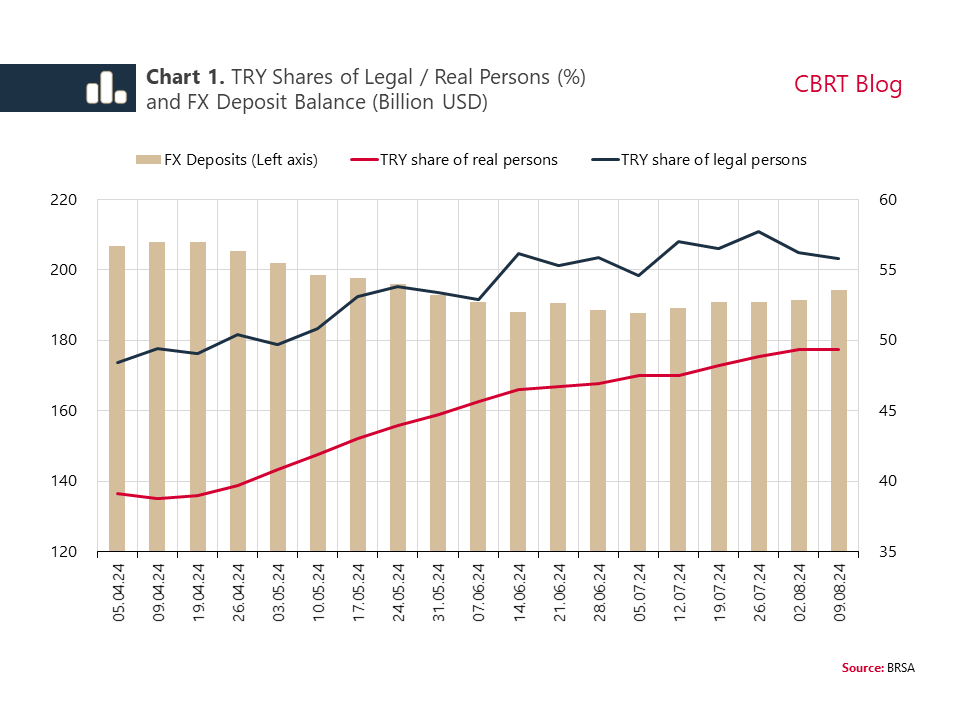

There was a rapid shift in preferences towards Turkish lira deposits in April and May due to the tightening steps taken in March. As a result, the FX deposit balance decreased from USD 210 billion to USD 190 billion by early June. During this period, the share of TRY deposits held by individuals and legal entities rose sharply (Chart 1).

In July and August, the rise in the TRY deposit share among individuals has continued, albeit at a slower pace. This slowdown is expected as the TRY share approaches historical averages (60%). On the other hand, the TRY deposit share among legal entities, which has surpassed historical averages (49%), is now relatively stable.

In a setting where preferences for TRY are strengthening, posting a current account surplus during summer months may be one of the factors driving the increase in FX deposits. During the summer months, when the economy typically runs a current account surplus, companies might seasonally increase their FX deposits. Another important factor contributing to the rise in FX deposits is the accelerated exit from KKM, driven by recent policy measures.

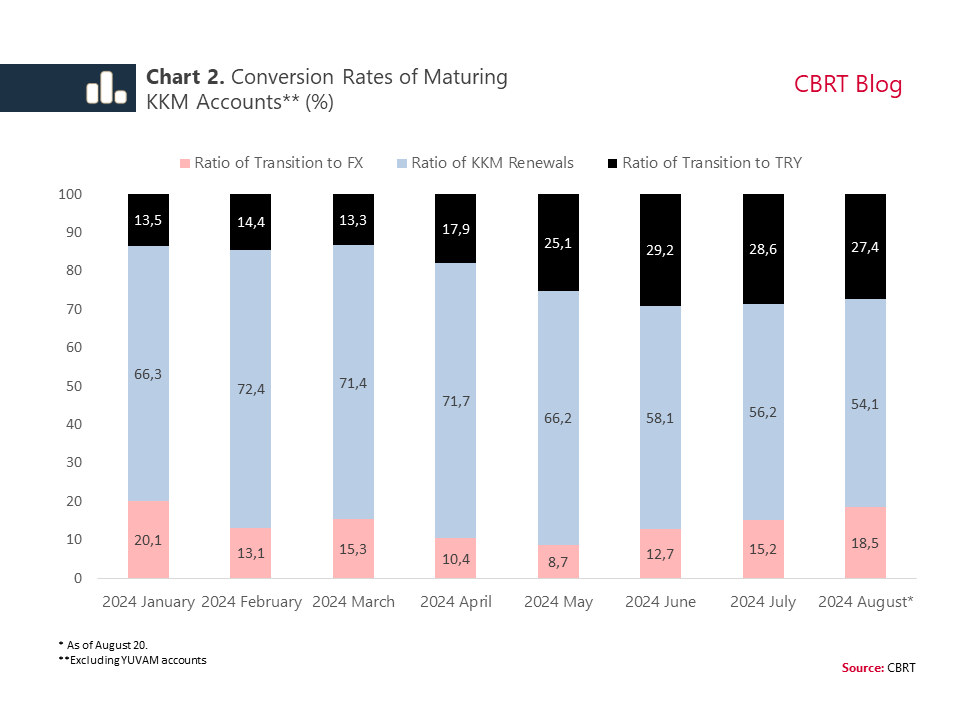

Beginning in April 2024, the decline in KKM accounts gained pace, driven by both residents’ and non-residents’ increased demand for Turkish lira assets, improvements in central bank reserves, and the CBRT’s efforts to curb the KKM supply and demand. Tax regulations on KKM accounts introduced by the Ministry of Treasury and Finance also supported this process.

The decline in KKM renewals on the back of incentives to reduce the KKM balance amid these regulations led to an increase in the transitions to TRY and FX at maturity (Chart 2). These shifts align with the CBRT’s expectations and the objectives of the regulations. In the last two months, the KKM balance fell by over USD 14 billion, with approximately USD 4.7 billion being withdrawn and invested in FX or gold at maturity.

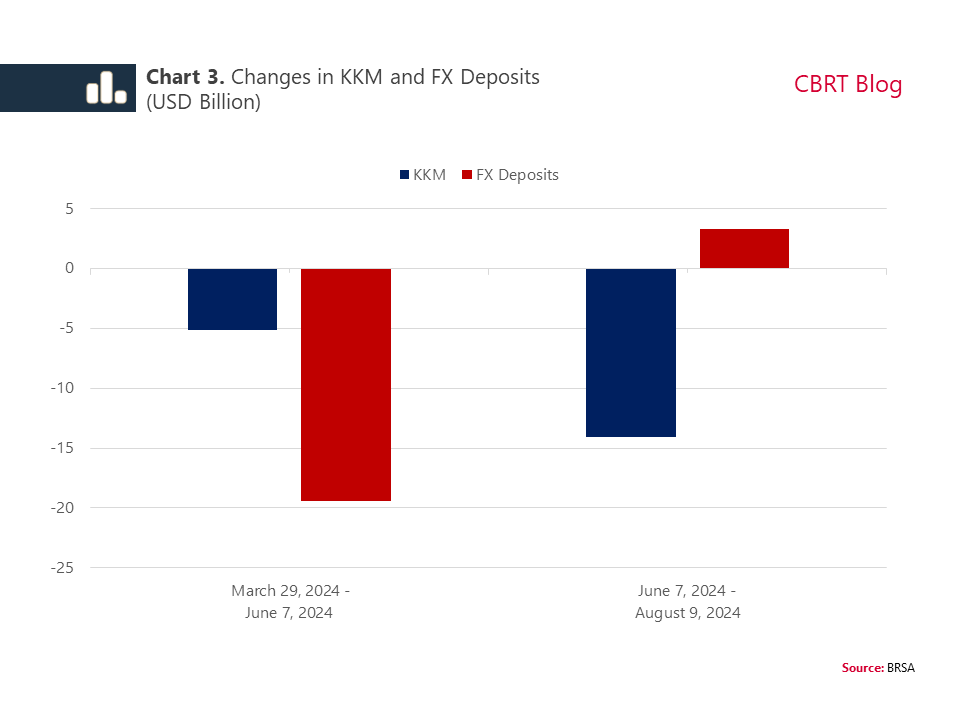

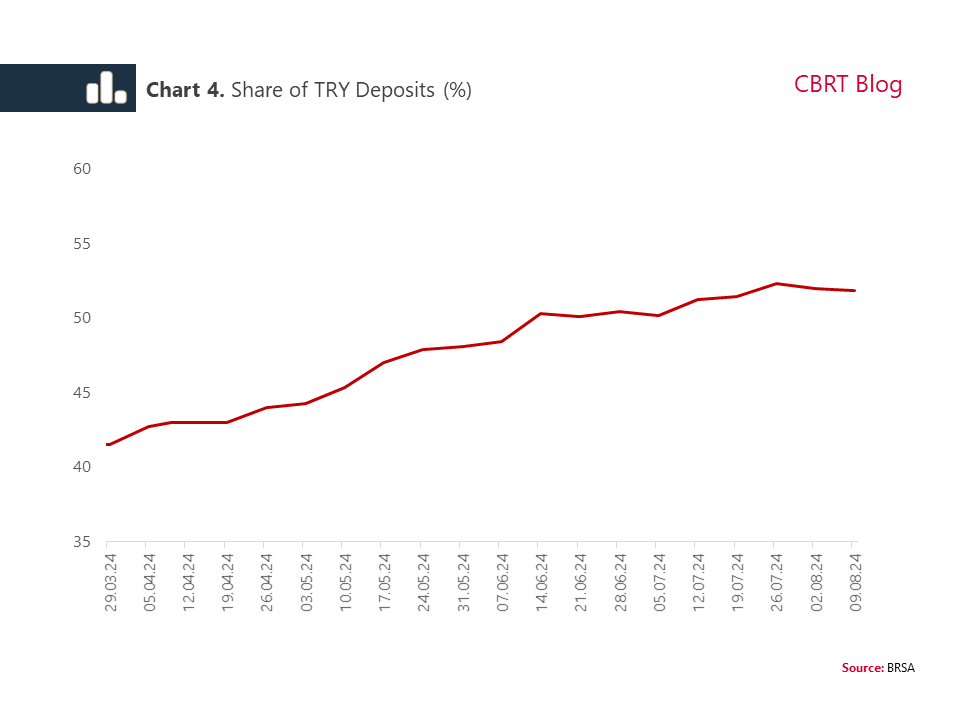

Despite the unwinding of USD 14 billion in KKM balances, FX deposit balances increased by only USD 3.3 billion in the last two months. Analyzing the combined total of KKM and FX deposits, we observe that the overall decline continues (Chart 3). In fact, the share of TRY deposits in total deposits increased from 48.4% to 51.8% over the last two months (Chart 4). Following a rapid shift from FX deposits to TRY deposits, the FX deposit balance is stabilizing amid the accelerated exit from KKM. The decline in inflation over the next months will further boost the rise in the share of TRY deposits.

[1] Foreign currency deposits refer to FX deposit accounts and precious metal deposit accounts.