In terms of monitoring and measuring the sovereign risk, credit default swap (CDS) premia act as an important indicator traded in financial markets. CDS contracts are derivative instruments that are written on fixed-income securities and enable transfer of credit exposure or taking a speculative position. CDS contracts can be written on corporate bonds, asset-backed securities and bonds issued by sovereign entities, but the most liquid ones are contracts on emerging market sovereign bonds.

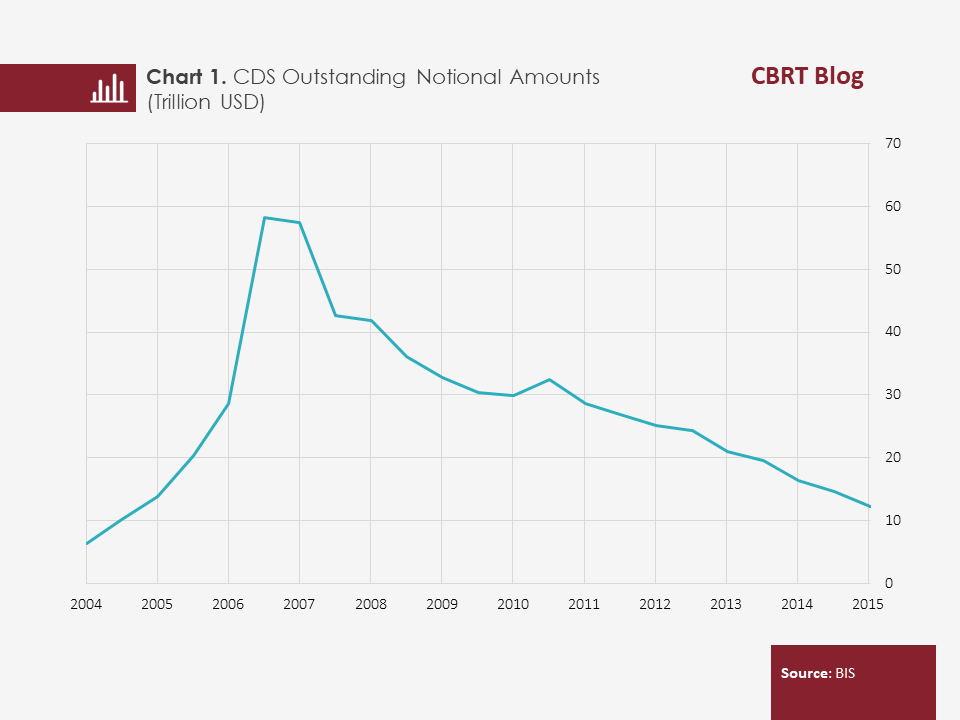

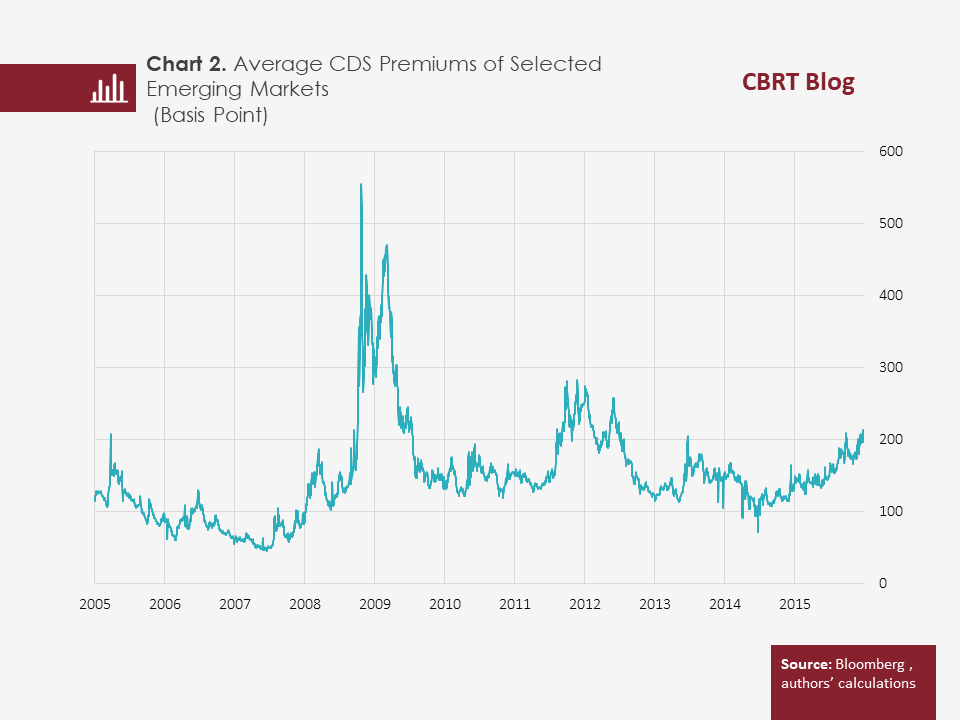

In terms of nominal values, the use of CDS contracts has become widespread in the last 20 years (Chart 1). During periods such as the Global Financial Crisis and the European Sovereign Debt Crisis when there were unexpected upswings in credit risk and losses in the values of financial products, CDS premia of emerging market economies (EMEs) increased sharply (Chart 2). Another observation is that the risk premia of peer countries tend to move together. This suggests that the course of risk premia may be affected by common global factors. Considering that credit risk premia provide an input in asset pricing, high sensitivity to global factors may disrupt pricing and weaken the monetary policy transmission mechanism. Therefore, identifying the factors that affect credit risk premia and developing appropriate policies are deemed to be crucial to support the proper functioning of financial markets.

Although EME credit risk premium indicators are simultaneously affected by global factors, they may still vary across countries. This situation has also been discussed in the academic literature (Amstad et al., 2016). This blog post analyzes macroeconomic and global variables that may lead to such cross-country differences. Detailed results are presented in Çepni et al. (2017). The country set is composed of Chile, Colombia, Mexico, Hungary, Peru, Poland, South Africa and Turkey while the sample period covers the years between 2005 and 2015. The principal component analysis (PCA) has been utilized to explain the co-movement of sovereign risk premia. The results indicate that the first two factors explain approximately 83 percent of the variation in CDS premia. When the PCA is repeated with rolling windows, the explanatory power of the first two factors also remains high over time.

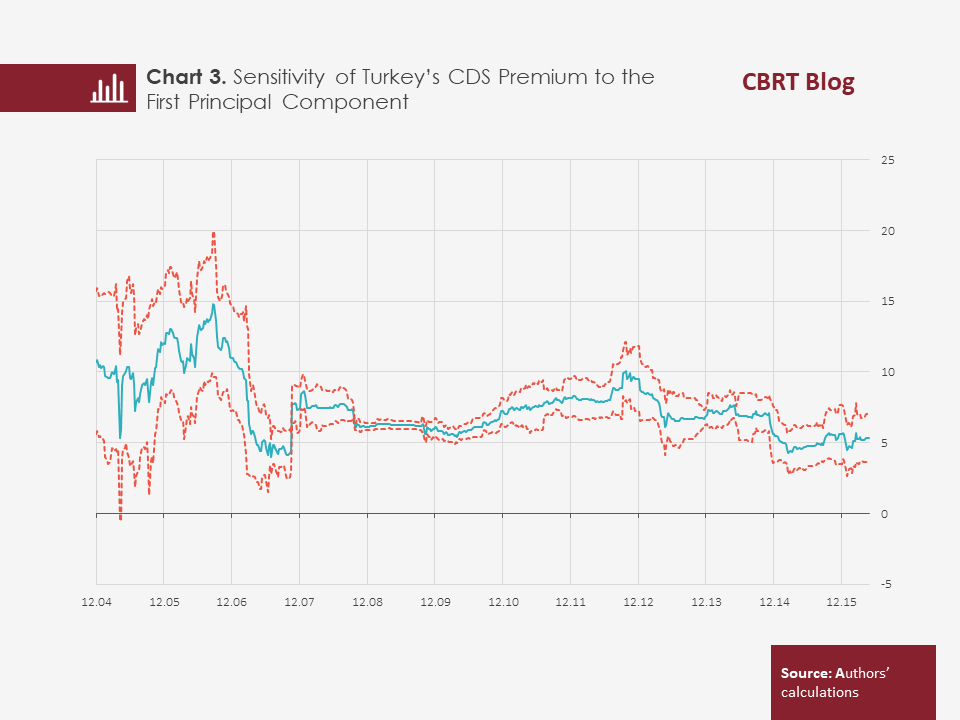

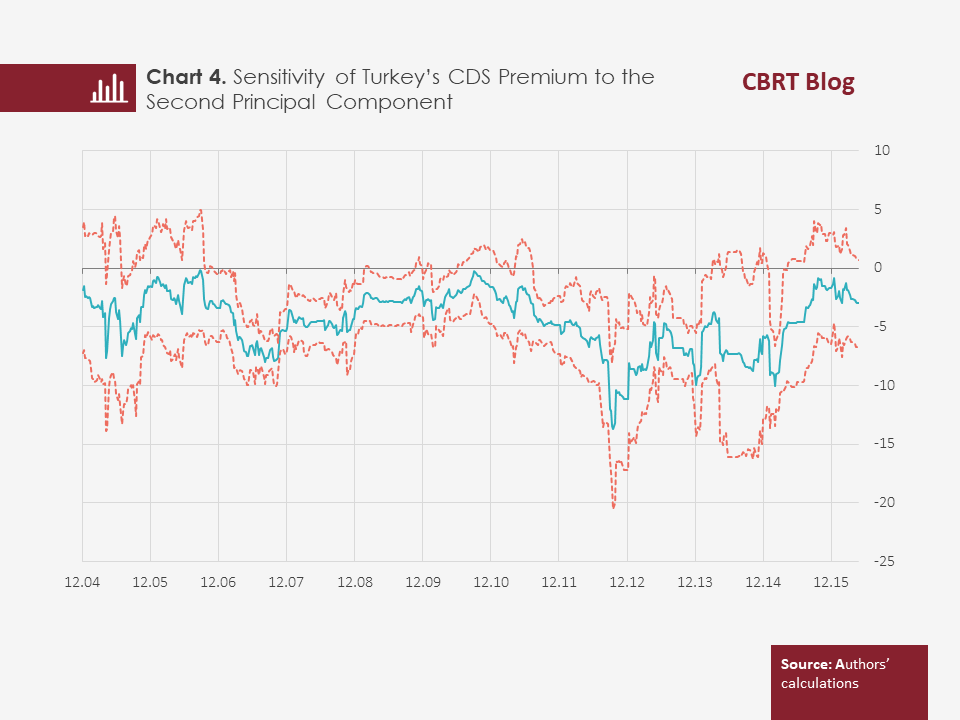

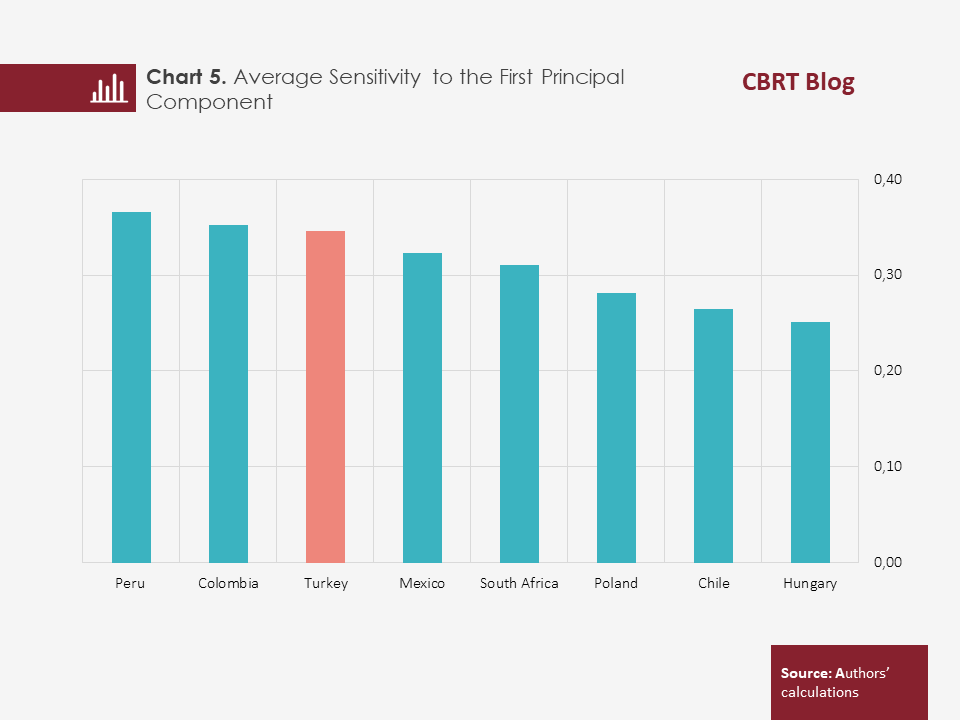

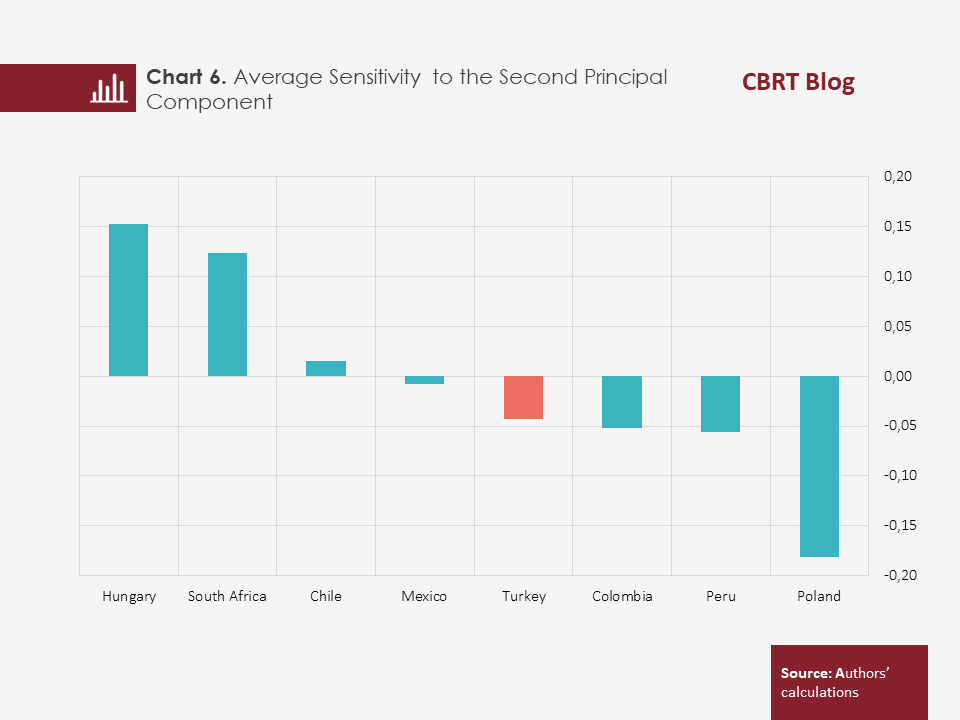

In the second step, the sensitivity of changes in each country’s credit risk premium to principal components is calculated via rolling regressions. In this way, the sensitivity of countries to common risk factors is analyzed. While the sensitivity to the first risk factor takes positive values for all countries during all episodes, the sensitivity to the second risk factor changes sign over time. Since the sensitivity to the first risk factor takes the same sign for all countries, this variable can be considered a global risk factor. Turkey’s sensitivity to the global risk factor is also found to increase during crisis times, with the confidence band getting narrower.

The variation in the sensitivity to the global risk factor across countries shows that global investors do not consider the bond markets of EMEs a single asset class and differentiate between these countries based on country-specific factors (Chart 5). On the other hand, the sensitivity to the second principal component changes sign across countries and its size remains relatively low (Chart 6).

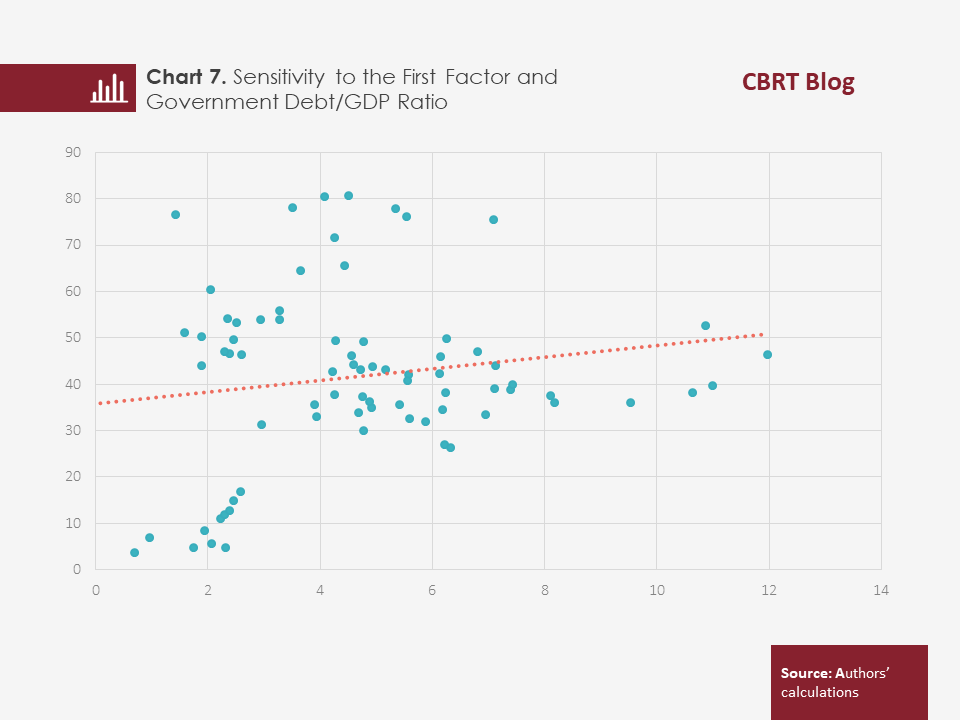

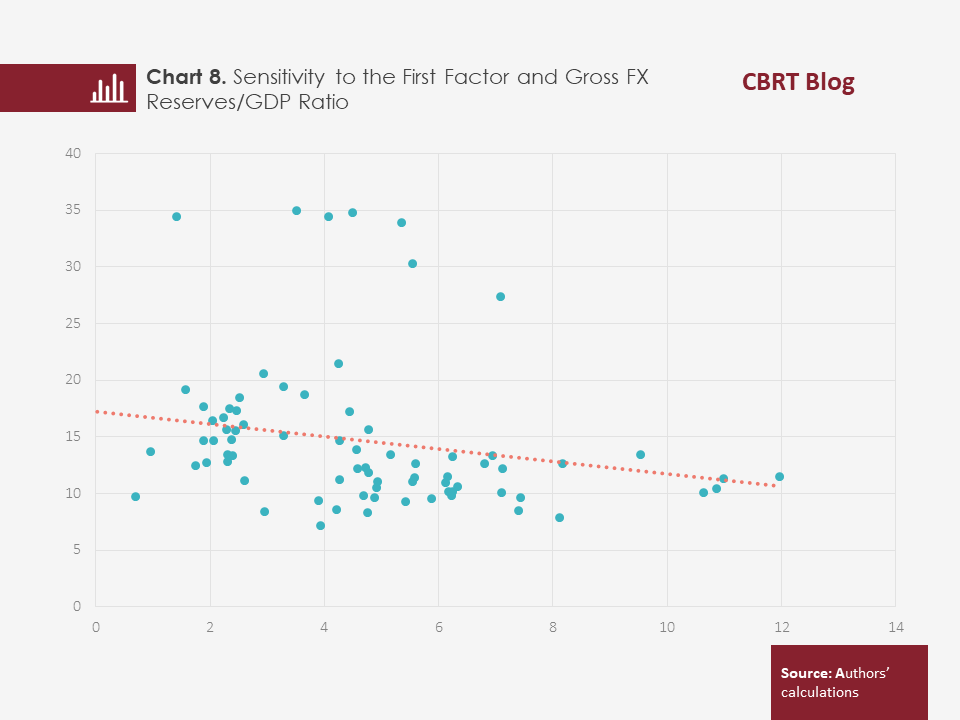

The differentiation of the sensitivity to the principal component defined as a global risk factor across countries and time raises the question of which factors may affect this sensitivity. In this scope, employing the panel regression model, we explain the sensitivity to the global risk factor via macroeconomic variables frequently used in the empirical literature to explain the movements in CDS premia. The data set includes information on variables such as growth, inflation, current balance, foreign trade volume, budget balance, government indebtedness, net international investment position and FX reserves. Running the fixed-effects model, we find that the government indebtedness and FX reserves variables have a statistically significant effect on the sensitivity to the global risk factor. In other words, we find that the credit risk premia of EMEs with lower government debt and higher FX reserves are less sensitive to changes in global financial conditions and the risk appetite (Charts 7 and 8).

To sum up, results of our analysis demonstrate that low government debt and adequate FX reserves positively affect the perception of sovereign risk in financial markets. In this respect, recent policy steps towards effective use of reserves are thought to be beneficial. The cessation of auctions for FX selling against TL by the CBRT in 2016 and the policy for reserve accumulation via export rediscount credits are important in terms of increasing the resilience to external shocks. Moreover, FX Deposits against TL Deposits Auctions and TL-Settled Forward FX Sale Auctions are considered complementary instruments contributing to the effective use of reserves in this context.

Bibliography

Amstad, M., Remolona, E., & Shek, J. (2016). How do global investors differentiate between sovereign risks? The new normal versus the old. Journal of International Money and Finance, 66, 32-48.

Cepni, O., Kucuksarac, D., & Yilmaz, M. H. (2017). The Sensitivity of CDS Premium to the Global Risk Factor: Evidence from Emerging Markets (No. 1704). Research and Monetary Policy Department, Central Bank of the Republic of Turkey.