The final draft of the tax reform proposal aiming at cutting tax rates in the United States (US) was passed by the US Congress last December and signed into law on 22 December 2017. This blog post discusses the potential effects on economic growth of the new tax law, also known as the Tax Cuts and Jobs Act, which became effective as of 1 January 2018.

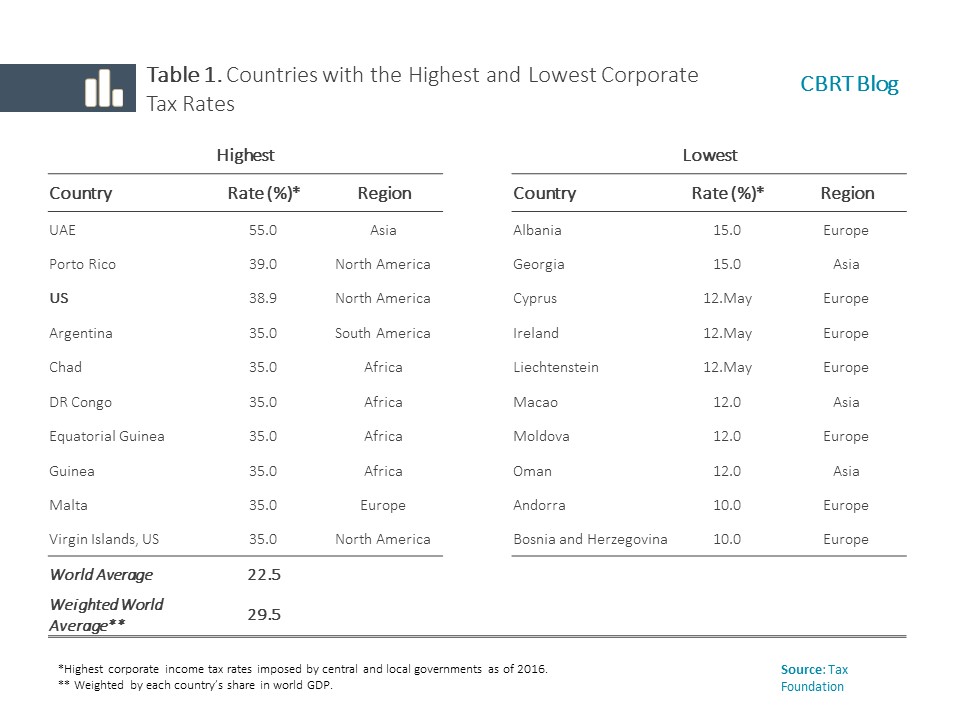

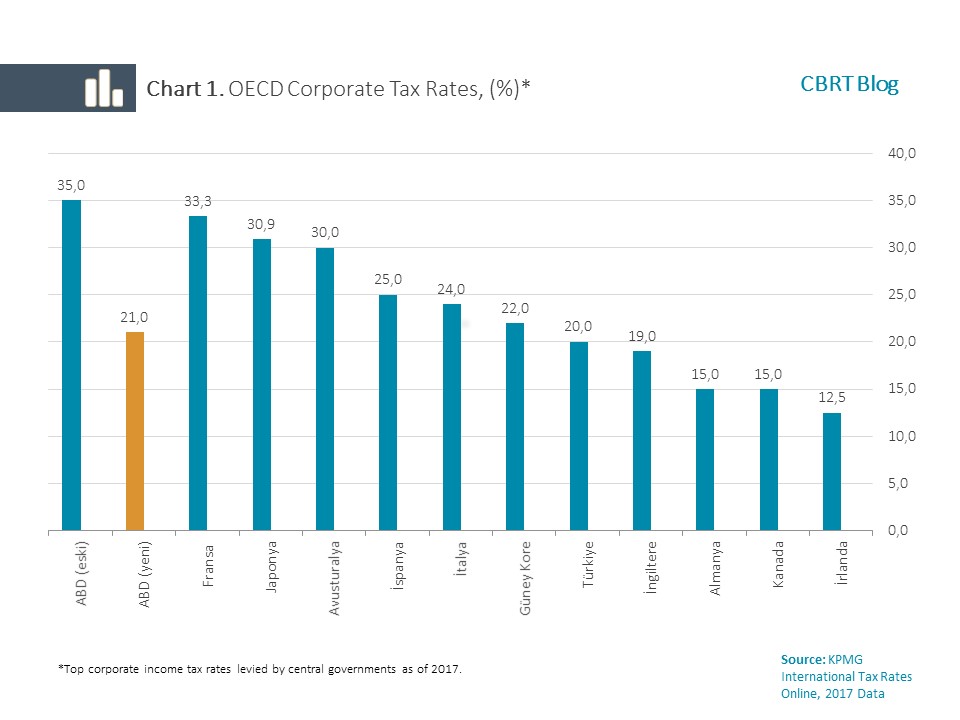

In the pre-reform period, the US had the third highest top statutory corporate tax rate in the world, at about 39 percent (Table 1). If the comparison is confined to corporate taxes levied by central governments, the US ranked first among OECD countries (Chart 1). The new tax law permanently slashed top corporate income tax rate from 35 percent to 21 percent. This reform aims to stimulate domestic investments and bring back investments held overseas due to high tax rates and, therefore, is expected to boost economic growth and employment (Feldstein, 2017).

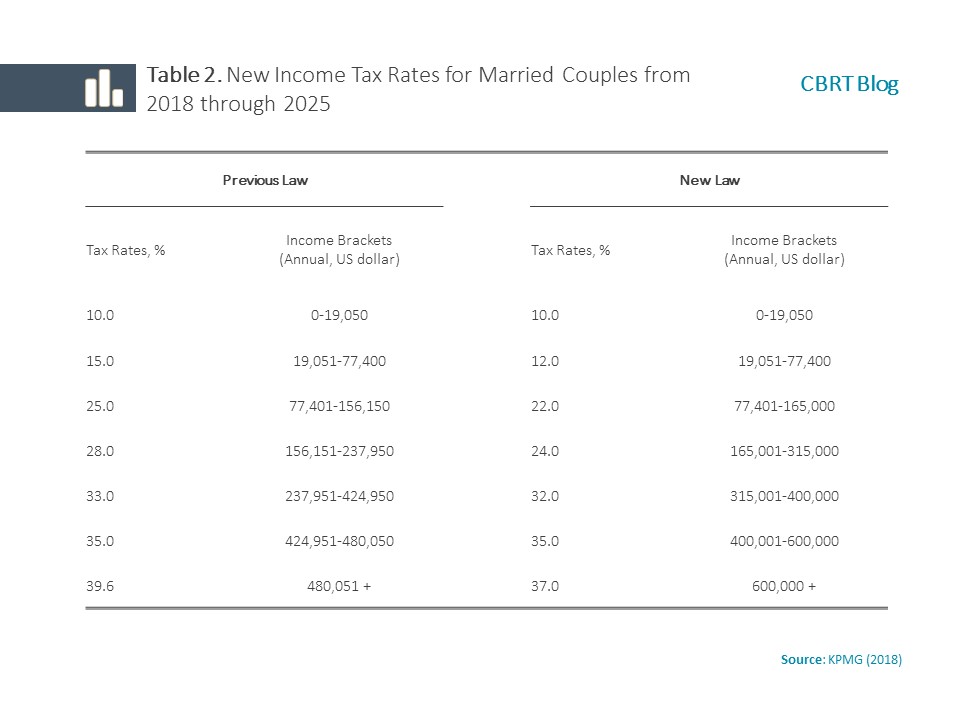

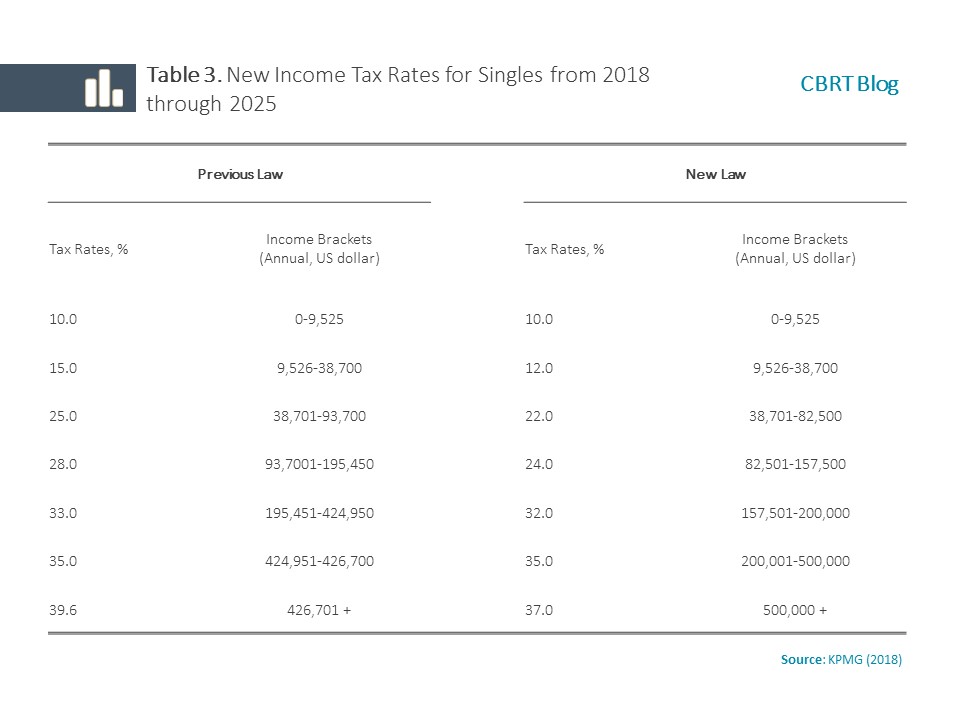

The new tax law also introduced temporary reductions in the individual income tax rates.[1] As seen in Table 2 and 3, the new tax law both widens the tax brackets for low and middle-income earners and reduces corresponding rates. Therefore, it is possible to say that the new legislation has reduced the tax burden on middle-income households and brought some fairness to the tax system, which is expected to broaden the tax base.

The tax reductions under the new tax law will undoubtedly increase the budget deficit in the short run. However, as it promotes economic growth and, thus, income, many believe that the new law will have a positive impact on tax revenues and the budget balance in the medium and long term (Feldstein, 2018).

Theoretical Framework

In Economic theory, the effects of tax cuts on economic growth is assessed in the framework of supply side gains. Therefore, it is important to distinguish between short-term demand effects and long-term supply effects of tax reductions. According to economic theory, the supply-side effects of tax reductions on growth occur as follows:

- According to the neoclassical theory of investment, a decrease in the corporate income tax rate lowers the user cost of capital and boosts a firm’s desired level of capital stock and, thus, investment demand (Hall & Jorgenson, 1967). Moreover, a reduction in the corporate income tax can increase a firm’s current and expected cash flow and therefore have a positive impact on investments (Lewellen & Lewellen, 2016).

- To promote economic growth, a reduction in personal income tax rate should encourage individuals to work and save much more. Yet, this only happens if labor supply rises after tax cuts. Theoretically, a tax cut in personal income has two distinct effects on labor supply: substitution effect and income effect. The substitution effect induces individuals to work more hours while the income effect induces them to work less. Therefore, a reduction in personal income tax rates may have a positive effect on labor supply and, thus, on savings and investments only if the income effect is small or negligible.[2]

- Both theoretical and empirical studies have found that if increased budget deficits following tax cuts are financed by prolonged borrowing, then they would adversely affect economic growth (Barro, 1988; Bräuninger, 2005; Ueshina, 2018).

- Reductions in the corporate income tax lower the user cost of capital and therefore attract foreign direct capital investments into the economy. Direct capital investments could be either in the form of investments by foreign companies or the return of domestic capital that fled abroad to avoid high corporate taxes.

Assessment and Conclusion

The new tax legislation enacted in the US is expected to boost economic growth by promoting investment profitability and capital accumulation. In addition, repatriating stockpiled profits and investments parked overseas to avoid high corporate income taxes will be another key factor triggering capital accumulation.[3] More importantly, new investments are expected to increase productivity and thus ensure a permanent growth surge, thereby pushing up real wages amid productivity gains (Feldstein, 2018).

However, the new law also raised some concerns about how it will affect economic growth positively:

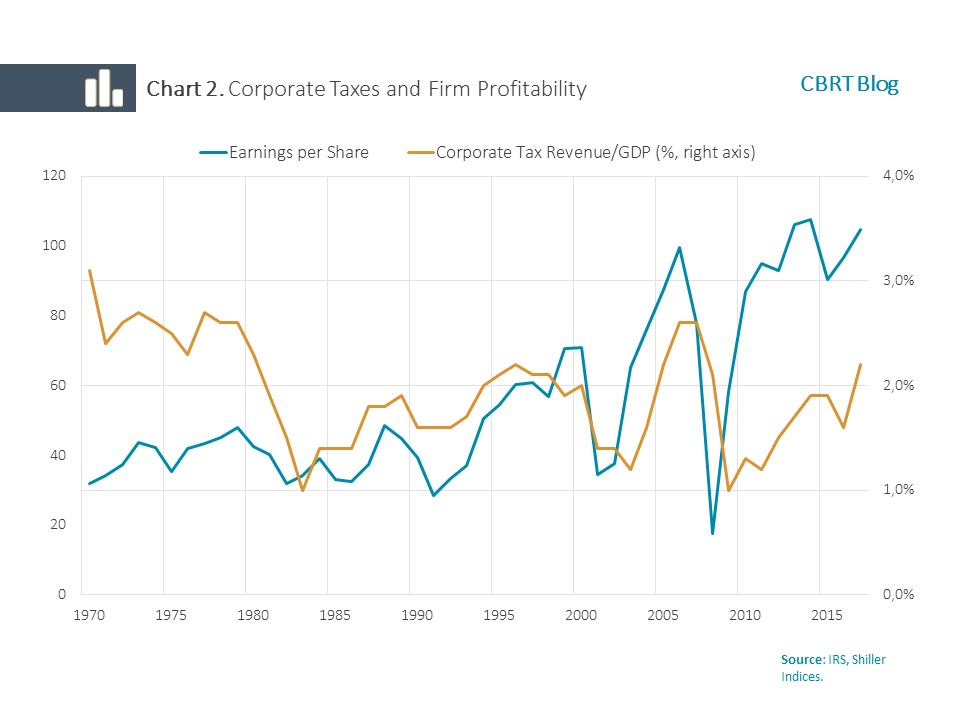

- Currently, firms experience historically high after-tax profits in the US (Chart 2). Likewise, interest rates are historically low In spite of low interest rates and high profit margins, the low levels of investment indicate a shortage of demand rather than a savings deficit.

- The budget deficit has started to increase recently in the US and, moreover, the debt-to-GDP ratio climbed over 100 percent, hovering at record highs (Chart 3). Therefore, although tax cuts raise economic growth in the short run by stimulating domestic demand, they may depress economic growth in the medium and long run by worsening the US fiscal balance and thus raising borrowing costs.

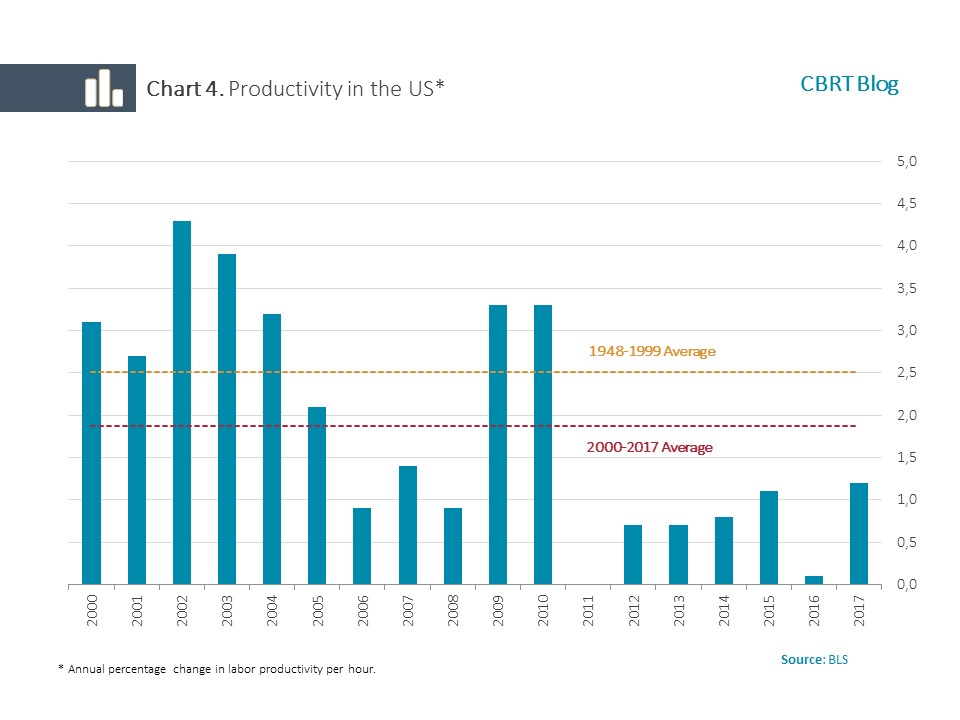

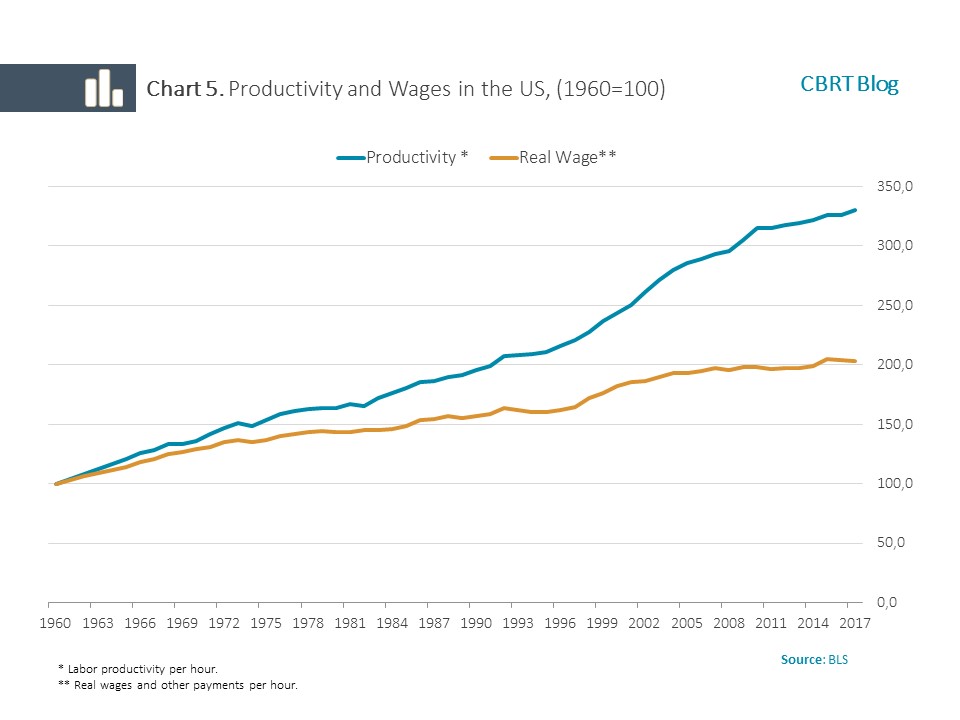

- It is not likely that increased investments in the aftermath of new tax law lead to increase productivity growth. In fact, the rate of productivity growth has been decelerating considerably in the US since mid-2000s due to structural and demographical factors (Chart 4). [4] Therefore, increased investments stemming from tax cuts may not accelerate productivity growth. Moreover, even if new investments boost productivity, this may not fully pass through to real wages. Because the relationship between productivity and wages has been drastically weakened in the last twenty years in the US economy (Chart 5).

In conclusion, it is possible to say that the new tax law will stimulate US domestic demand and promote economic growth in the short run. Its medium and long-term impact will be determined by the supply-side effects, which eventually depends on the magnitude of its impact on capital accumulation, the composition of investments and, of course, preventing fiscal deterioration. In addition, according to the economic literature, convergence of an economy to its long-run equilibrium can be quite slow (Barro & Sala-i-Martin, 2005). In this context, the initial supply-side effects of the new US tax law is highly likely to be e positive, but it is worth reminding that there are significant uncertainties on transmission mechanisms over the medium and long term.

[1] The new arrangements on individual income tax rate are scheduled to 31 December 2025.

[2] A study on the effects of the tax acts of 1981 and 1986 on labor supply in the US concluded that reductions in income tax had little positive impact on labor supply (Bosworth & Burtless, 1992).

[3] US-origin international companies stockpiled offshore profits to avoid taxes in the US. These profits are estimated to be around 2.1 trillion US dollars as of 2015 (Rubin, 2015).

[4] The slowdown in productivity growth is not a US issue. Economists have failed to offer a sufficient explanation for the slowdown that also occurs in advanced economies, particularly in the EU (Jones, 2017).

References:

Barro, R. (1988), The Ricardian Approach to Budget Deficits. Journal of Economic Perspectives 3(2): 37-54.

Barro, R. ve Sala-i-Martin, X. (2005), Economic Growth. MIT Press, Cambridge, USA and London, UK.

Bosworth, B. ve Burtless, G. (1992), Effects of Tax Reform on Labor Supply, Investment, and Saving Journal of Economic Perspectives, 6(1): 3-25

Bräuninger, M. (2005), The Budget Deficit, Public Debt, and Endogenous Growth. Journal of Public Economic Theory, 7: 827-840.

CBO (2017), An Analysis of Corporate Inversions. Congressional Budget Office, September 18: https://www.cbo.gov/publication/53093

Feldstein, M. (2017) Tax Reform and Budget Deficits in America, Project Syndicate, 29 Ağustos: https://www.project-syndicate.org/commentary/us-tax-reform-and-budget-deficits-by-martin-feldstein-2017-08?barrier=accessreg

Feldstein, M. (2018), The Tax Reform Legislation of 2017. Journal of Policy Modeling Yayımlanma sürecinde.

Lewellen, J. ve Lewellen, K. (2016), Investment and Cash Flow: New Evidence Journal of Financial And Quantitative Analysis 51(4): 1135-1164.

Jones, C. I. (2017), The Productivity Growth Slowdown in Advanced Economies, ECB Forum on Central Banking, June: https://web.stanford.edu/~chadj/JonesSintra2017.pdf

Jorgenson, D. ve Hall, R. E. (1967), Tax Policy and Investment Behavior. American Economic Review 57(3):391-414.

KPMG (2018), Tax Reform-KPMG Report On New Tax Law: Analyis and Observations, February 6: https://www.google.com/search?q=KPGM+tax+reform&ie=utf-8&oe=utf-8

Rubin, R. (2015), U.S. Companies Are Stashing $2.1 Trillion Overseas to Avoid Taxes, Bloomberg, March 4: https://www.bloomberg.com/news/articles/2015-03-04/u-s-companies-are-stashing-2-1-trillion-overseas-to-avoid-taxes

Ueshina, M. (2018), The Effect Of Public Debt On Growth And Welfare Under The Golden Rule Of Public Finance. Journal of Macroeconomics, 55:1-11.