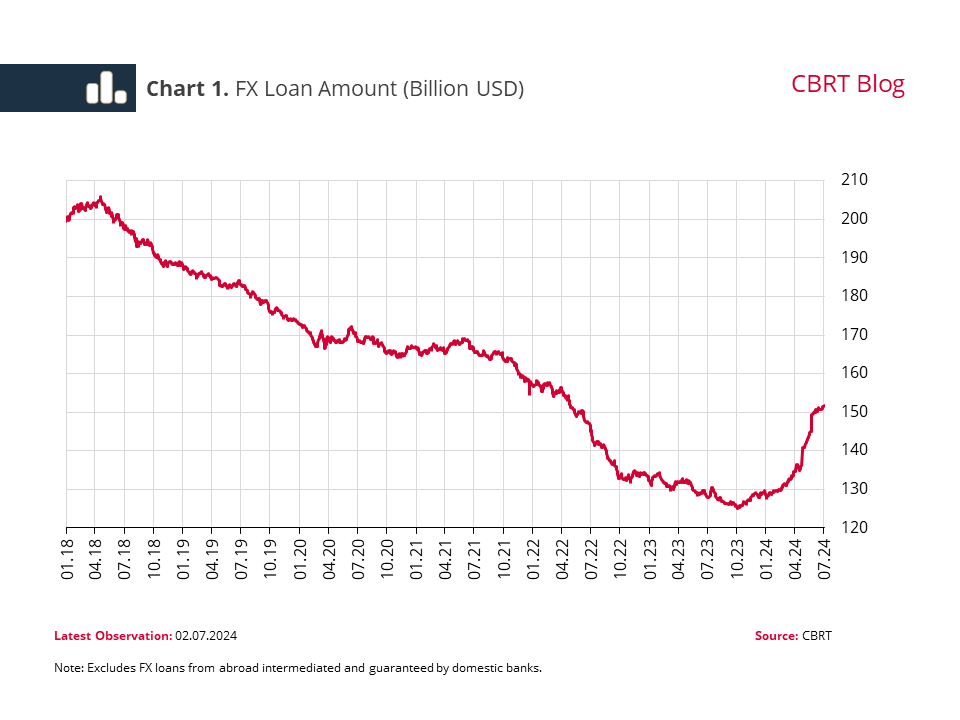

Development and composition of loans are important to domestic demand conditions, as well as to price and macrofinancial stability. Following a decline after 2018, foreign exchange (FX) loans have recently assumed an upward trend. Subsequent to this uptick, the Central Bank of the Republic of Türkiye (CBRT) took additional tightening steps in support of the tight monetary policy. On 23 May 2024, reserve requirements were introduced to FX loans in excess of a monthly growth limit of 2%, excluding loans for investment purposes, a move designed to restrict FX loans. This study examines the dynamics of the recent increase in FX loans and analyzes the developments in loan maturities in view of supply/demand-side factors.

The rate spread between TL and FX loans widened during the monetary tightening cycle that started in the second half of 2023. Backed also by the improved exchange rate expectations, FX-denominated loan demand of firms increased. In the same period, banks found that borrowing conditions from international markets had become less stringent and the share of external FX debts within total liabilities went up. Banks’ FX liquidity position grew stronger due to the CBRT’s currency swap transactions and rising capital and cash inflows. These supply and demand-side components underpinned FX loans (Chart 1).

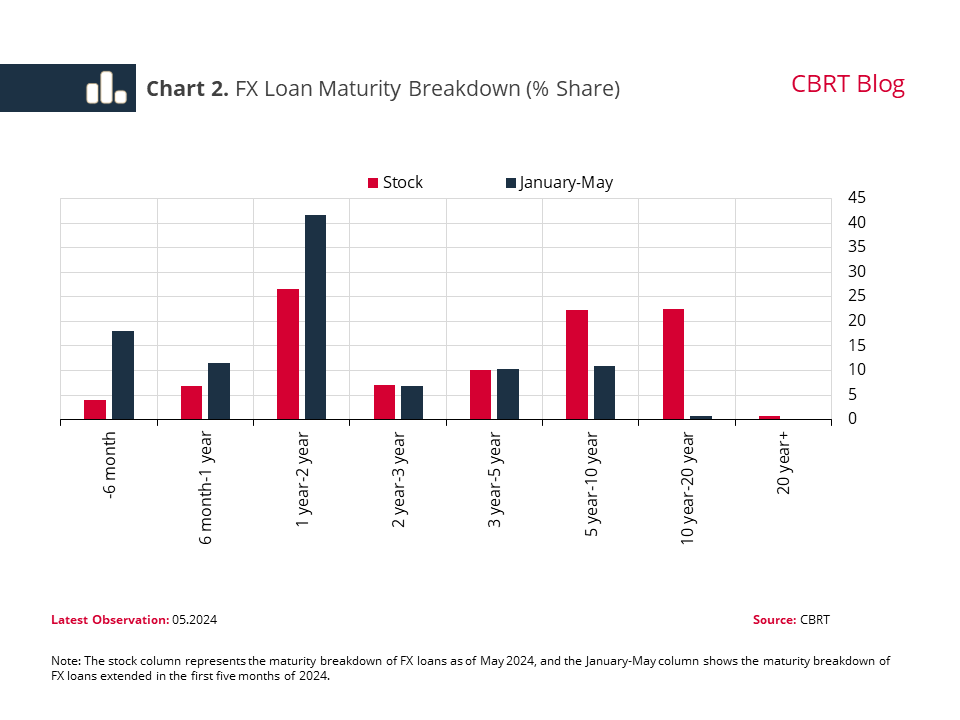

Both the growth rate of loans and their maturity composition are significant to financial stability. Long-term loans are mostly utilized for investment purposes and bolster financial stability by ensuring firms are affected less by possible changes in loan standards caused by shifting business and financial cycles. In the period under examination, maturities shortened despite the rise in FX loans (Chart 2). This implies that FX loans, which have historically been extended for investment and project financing purposes, have recently been utilized to finance working capital. A firm-level data set was employed to determine the main driver of this trend.

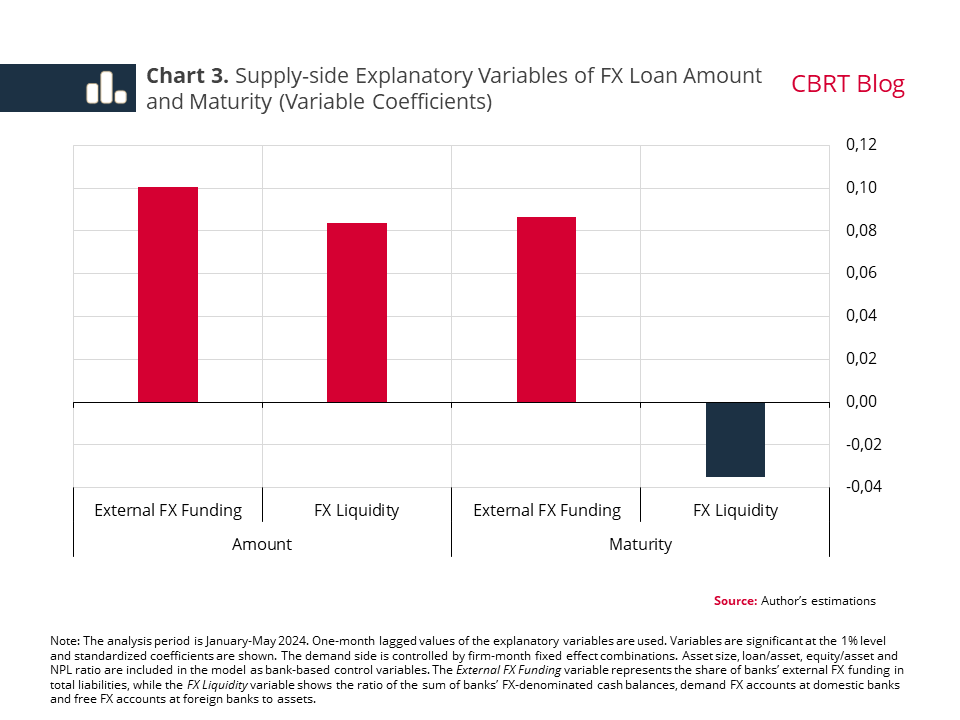

Supply-side factors are the focus of the model that control the firm demand. Results indicate a positive correlation between the shares of FX loan amount and external FX funding (Chart 3). On the other hand, there is a positive correlation between the FX loan maturity and the share of external FX funding, in contrast to a negative one with the FX liquidity. In other words, banks with a higher share of external FX funding extend higher amounts of FX loans with longer maturities. A one-point increase in the external FX funding rate pushes banks’ FX loan amount up by 0.8% and the maturity by 0.7%. However, it is notable that banks with higher FX liquidity extended higher amounts of FX loans with shorter maturities. A one-point increase in the FX liquidity ratio increases the FX loan amount by 3.6%, but shortens the maturity by 1.5%.

With a view to limiting the sensitivity to global liquidity developments and capital flows, the maturity extension of non-core FX liabilities and banks’ longer-term borrowing from abroad are supported by lower reserve requirement ratios. Findings show that the reserve requirement rule has affected the maturity of domestic FX loans, and banks borrowing from abroad in higher amounts have extended higher amounts of FX loans with longer maturities.

Moreover, results imply that the main driver of the recent shortening trend in FX loan maturities has been the developments in banks’ FX liquidities. Increased FX liquidity of banks has led to higher amounts of FX loan supply with shorter maturities.

In sum, there is a positive correlation between the amount of FX loans and external borrowing and FX liquidity, while FX loan maturities get shorter along with the strengthening FX liquidity of the sector. In addition, firms’ elevated exchange rate risk also constitutes a potential risk to financial stability. Accordingly, utilization of FX loans for investment purposes with longer maturities is significant to the management of such risks in the medium-long term. The FX loan arrangement introduced in May exempting investment loans with a maturity longer than two years also serves this purpose.