Governor Murat Uysal's Speech at the Briefing on Inflation Report 2020-IV (İstanbul)

Distinguished Members of the Press, Esteemed Guests,

Welcome to the briefing held to convey the main messages of the fourth Inflation Report of 2020.

As usual, I will begin the briefing with a presentation covering our evaluations of the macroeconomic outlook and the monetary policy stance, as well as our revised inflation forecasts. Then I will answer your questions.

Before moving on to the macroeconomic outlook, I would like to point out the changes we made to the inflation report. The new version of the inflation report consists of three main chapters: overview, economic outlook and medium-term projections. The overview chapter starts with the macroeconomic outlook and then highlights our monetary policy actions over the reporting period before summarizing the key risks surrounding medium-term projections and forecasts. In the economic outlook chapter, we delve into the major developments of the relevant period under four headings, i.e. global economy, financial conditions, economic activity and inflation developments. As always, the final chapter includes our medium-term forecasts and risk assessments.

From now on, we will focus on details that we find circumstantially critical in the “Zoom In” sections. Besides, we continue to publish boxes that involve our thematic analyses and prevailing discussion topics of the period. The first box provides an evaluation of the factors that have recently been reducing the efficiency of monetary policy in emerging economies, while the second box explores the integrated policy framework suggested for emerging economies given such challenges. There is another study that discusses the Fed’s average inflation-targeting regime and its possible effects. Of the two boxes on domestic economic activity and inflation developments, the first gives a brief account of the short-term growth outlook with nowcasting models and high frequency indicators, while the other presents an analysis on the effect of aggregate demand conditions on inflation.

Esteemed Guests,

Now, I would like to continue my speech with the global and domestic macroeconomic outlook.

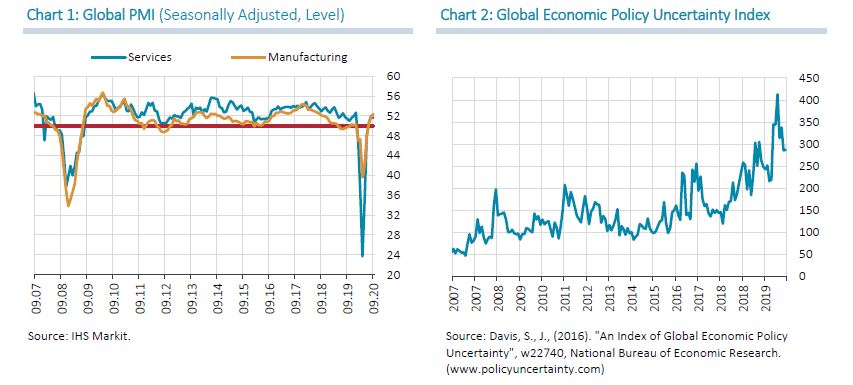

After hitting bottom in April in the aftermath of the coronavirus pandemic, the global economy saw some partial rebound following normalization steps. PMI indices, i.e. leading indicators for growth, continue to recover. However, global economic activity still remains below its pre-pandemic level. Although growth forecasts for 2020 have improved somewhat with incoming data compared to the previous reporting period, they still point to a significant contraction for the entire year (Chart 1). As of today, there remain uncertainties regarding the course of the pandemic and the effects of economic policies. Therefore, uncertainties over global economic recovery are high, which is confirmed by the wide-ranging growth forecasts (Chart 2).

On the inflation front, we see that energy prices remain low while commodity prices, especially international food prices, exceed their pre-pandemic levels. However, core inflation is significantly lower in advanced economies than before the pandemic. Due to weak growth and low inflation, advanced and emerging economies seem to maintain their expansionary monetary and fiscal stances (Chart 3). Despite increased global liquidity conditions and reduced returns on advanced market financial assets, high uncertainty discourages flows to emerging markets. We saw mostly outflows from emerging markets in the third quarter, while debt markets received some inflows in the final quarter (Chart 4).

Dear Guests,

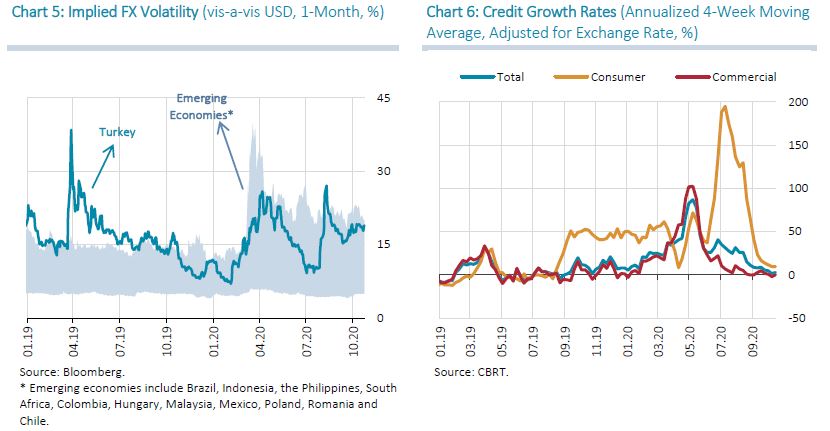

Despite the increase in global risk appetite following normalization, Turkey continued to see portfolio outflows in the third quarter. In addition, Turkey's risk premium remained volatile and high due to global uncertainties as well as country-specific factors. The widening current account deficit during the pandemic as well as portfolio outflows and repayments of matured external debt drove up the need for external finance, which caused exchange rates to be highly volatile (Chart 5). Despite tight external financing conditions, monetary and fiscal measures stimulated a rapid domestic credit expansion and the Turkish economy saw a rapid recovery.

Nevertheless, the impacts of this recovery called for a need to normalize the pandemic-specific policies in order to contain macrofinancial risks. Accordingly, as a result of the steps that the CBRT has been taking since August regarding the monetary policy and liquidity management as well as the coordinated normalization in macropolicies, a significant tightening has been achieved in financial conditions. Indeed, owing to the rise in loan rates, credit growth significantly slowed down at the end of the third quarter (Chart 6).

In the third quarter, financial conditions were supportive of the domestic demand, and economic activity posted a V-type recovery across a wide range of sectors (Chart 7). Nevertheless, this improvement remained limited in some goods and services sectors that had strong relations with the tourism sector, which was severely affected by the pandemic. High-frequency data suggest that the recovery continued in September and October as well (Chart 8). Domestic demand is expected to slow down in the upcoming period owing to the tightening in financial conditions, and we believe that the likelihood of a positive growth in 2020 without an additional policy support has increased.

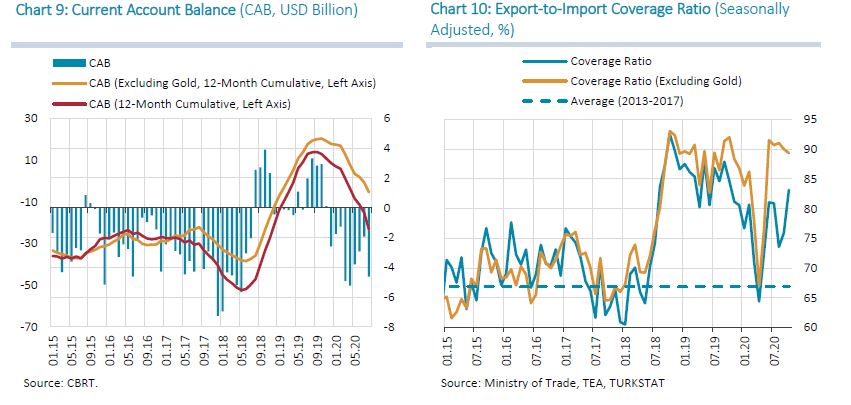

As for external balance, despite the stronger-than-projected recovery in exports of goods, there has been a rapid rise in the current account deficit because of the fall in services revenues, particularly in tourism revenues and the increase in imports. Exports recovered rapidly and exceeded the pre-pandemic level thanks to the normalization steps at the global scale and Turkey’s competitiveness in export markets. Owing to deferred demand conditions as well as liquidity and credit policies implemented within the scope of the coronavirus measures, import has assumed a recovery trend as of May. Moreover, due to global uncertainties and the recent dollarization trend, imports of gold increased rapidly and reached a historically high level in August. Thus, the current account deficit in the first eight months of the year was recorded at USD 26.5 billion (Chart 9). Excluding gold, export-to-import coverage ratio is historically high, showing that the real exchange rate level supports the adjustment in external balance (Chart 10). Accordingly, as the pandemic-specific credit policies normalize, we expect that the additional import demand stemming from strong credit acceleration would decrease and rebalancing effects of real exchange rates would become more apparent. Thus, the strong recovery in exports of goods and the relatively low level of commodity prices are expected to support current account balance in the upcoming period.

Distinguished Guests,

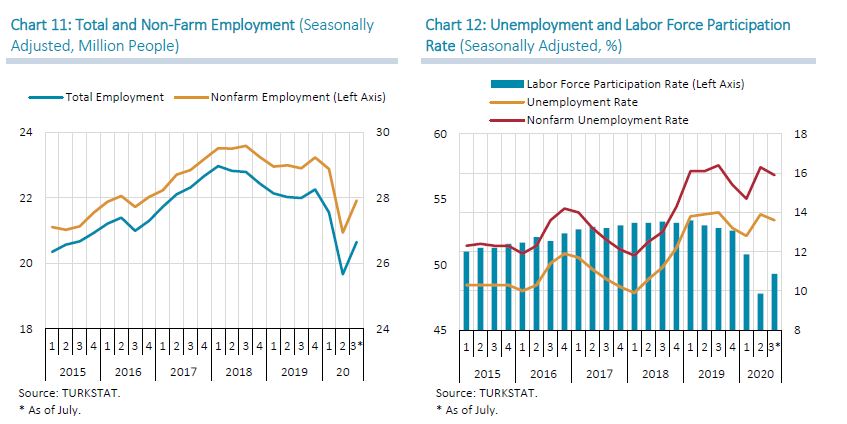

We have started to observe the positive effects of the strong recovery in economic activity on the labor market. In seasonally adjusted terms, only half of the job losses in the second quarter has been compensated so far (Chart 11). In this period, when job opportunities have decreased due to the pandemic, incentives such as short-term working allowance, as well as supports via unemployment insurance fund and current transfers played an important role in curbing household income losses. As of July, labor participation rate increased in tandem with the economic recovery while unemployment rates decreased (Chart 12). Leading indicators suggest that new job announcements have increased and employment opportunities have improved.

Dear Guests,

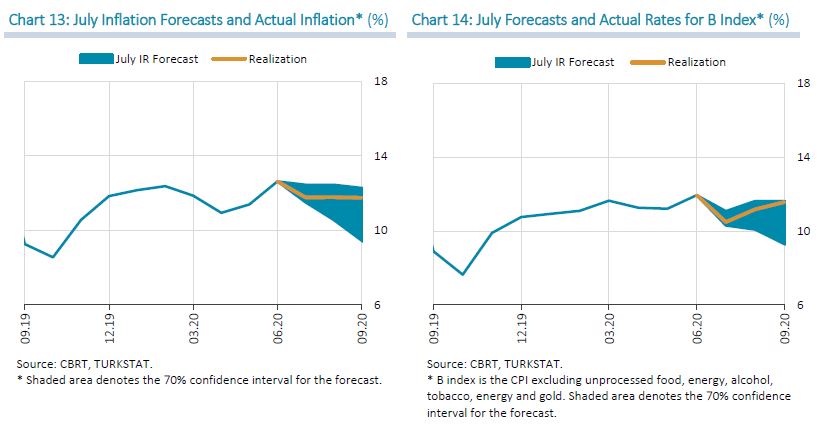

I would like to continue my speech with inflation developments. In the third quarter, consumer inflation and annual inflation of the B index –one of core indicators- were recorded at 11.75% and 11.57% and hovered close to the upper bound of the forecast range in the July Inflation Report (Chart 13 and 14). Despite our earlier evaluations that inflation would take up a downtrend in the second half on the back of stronger demand-driven disinflationary effects, inflation posted a higher-than-projected trend due to strong credit impulse and the depreciation in the Turkish lira.

Annual inflation in September was slightly lower compared to June. This decline was mainly driven by the base effect in alcoholic beverages- tobacco and energy groups (Chart 15 and 16). Although annual inflation moderately improved compared to the previous quarter and remained within the confidence interval, the outlook for the rest of the year suggests a higher trend than previous projections.

As a matter of fact, core indicators point to a core goods group-driven rise in the trend of inflation in the third quarter (Chart 17). Services display a relatively more moderate course (Chart 18). The high course in core goods inflation was led by exchange rate developments, as well as the durable goods group on the back of the strong credit impulse. Meanwhile, in the services sector that saw a pandemic-related rise in unit costs, the supply-side inflationary pressures decreased somewhat on the back of the normalization steps. The VAT cut on certain items was also instrumental in a lower inflation trend in services compared to the previous quarter. However, the high course in food inflation persists. Rising international food prices since August led to intensified cost pressures in the sector.

The rise in survey-based inflation expectations continued in the third quarter of the year (Chart 19). Despite a slight decline following the CBRT’s tightening steps, inflation compensation obtained from bond yields suggests that long-term inflation expectations and inflation uncertainty are still high (Chart 20).

Esteemed Guests,

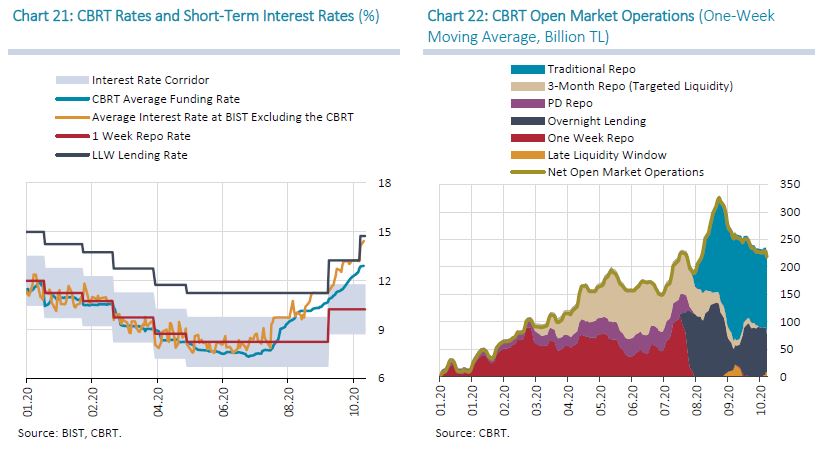

Since mid-July, considering the rebound in the economic activity and its reflections into macro balances, we have assessed that conditions have evolved to allow for gradual withdrawal of the pandemic-specific accomodative policy actions. Accordingly, we have started to take tightening steps in the context of liquidity management in August (Chart 21). In the same period, in line with the monetary tightening steps, the increase in the Turkish lira and FX reserve requirement ratios for banks fulfilling the real credit growth conditions became effective in a higher funding need in the system. A significant portion of the funding need was met through TL currency swap transactions. However, we changed the composition of funding through open market operations noticeably by gradually phasing out of the targeted liquidity facilities launched following the pandemic. In this period, while we decreased the share of funding through weekly and three-month repo auctions, we increased the amount of funding through overnight transactions and traditional auctions (Chart 22).

In September, we assessed that the tightening steps should be reinforced in order to contain inflation expectations and risks to the inflation outlook. In this period, we raised the policy rate by 200 basis points, and enabled a gradual increase in the weighted average funding cost in the following period. In October, we took another strong step towards tightening to restore disinflation process immediately. In this context, we changed the monetary policy operational framework and decided to enhance flexibility in liquidity management and set the margin between the CBRT Late Liquidity Window lending rate and overnight lending rate at 300 basis points. Under current circumstances, we formed a framework in which tight monetary stance will be maintained until the inflation outlook displays a significant improvement.

2. Main Assumptions and Forecasts

Dear Guests,

Before moving on to forecasts, I will briefly talk about our main assumptions.

We have based our medium-term projections on the macroeconomic outlook that I have summarized so far. Additionally, we have revised our assumptions for exogenous factors such as import prices, food prices and fiscal policy. Our assumptions for international crude oil prices were consistent with the projections of the July Inflation Report (Chart 23). Meanwhile, in view of the course of commodity prices such as industrial metal and agricultural product prices, we revised upwards our assumption for US dollar-denominated import prices for 2020 and 2021 (Chart 24). Moreover, we revised our food inflation forecast, which had been set at 10.5% in the July Inflation Report, upwards to 13.5% considering the recent trends in unprocessed food prices, exchange rate developments and the rise in international food prices. We also revised our food inflation forecast for 2021 to 10.5% from 8%. Our projections are based on a medium-term outlook in which fiscal and financial policies will be determined in tandem with the monetary policy, and in line with the projected disinflation path. In this scope, we have assumed that in addition to the administered price, tax and wage adjustments, the fiscal stance and credit policies will largely be set to support the disinflation process.

Dear Guests,

Now I would like to present our inflation and output gap forecasts based on the framework I have described so far.

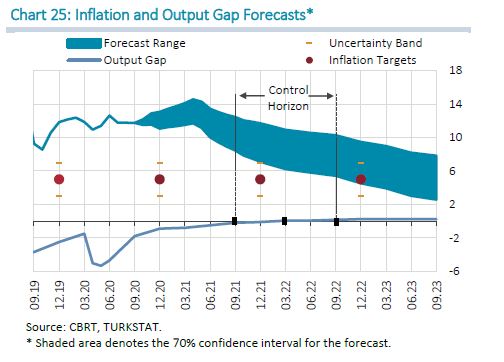

Under the current monetary policy stance and strong policy coordination, we foresee that inflation will converge gradually to the targets. Accordingly, we estimate that inflation will be 12.1% at the end of 2020 and fall to 9.4% at the end of 2021, before stabilizing around 5% over the medium term. With a 70% probability, inflation will be between 11.1% and 13.1% (with a mid-point of 12.1%) at end-2020 and between 7.1% and 11.7% (with a mid-point of 9.4%) at end-2021 (Chart 25).

In the July Inflation Report, we had judged that the pandemic-driven supply-side factors affecting inflation would phase out in the normalization period and demand-side disinflationary effects would become more prevalent in the second half of the year. However, as the normalization is taking place in a gradual manner, the pandemic-led supply-side inflationary effects persist, albeit getting milder, in the second half of the year. While aggregate demand conditions continue to restrain inflation in certain sectors, goods that are sensitive to financing conditions are registering large price hikes due to the strong credit impulse. Against this background, output gap forecasts have been revised upwards as of the second quarter of 2020.

I would like to continue my speech with an account of the factors that led us to make an upward revision in the year-end inflation forecasts for 2020 and 2021 in light of the recent inflation realizations and all factors affecting the inflation outlook.

We have revised the year-end inflation forecast for 2020 up by 3.2 points to 12.1% from 8.9%. The revision in Turkish lira-denominated import prices has driven up the consumer inflation forecast by 1.6 points, while the revision in the output gap has increased the inflation forecast by 0.9 points. The rise in the food inflation forecast has pushed the inflation forecast up by 0.7 points, while the revision in the underlying trend of inflation and initial conditions has been calculated to have an effect of 0.2 point. Meanwhile, we have assessed that the VAT cuts in the services sector will have an impact of minus 0.2 points on the year-end inflation forecast.

We have also revised the year-end inflation forecast for 2021 to 9.4% from 6.2%. The revision in the 2020 inflation forecast as well as import costs constitute the main drivers of this 3.2-point revision. The revision in the year-end inflation forecast for 2020 has raised the year-end inflation forecast for 2021 by 1.6 points through its impact on the backward-indexation behavior and the underlying trend of inflation. The assumption for Turkish lira-denominated import prices and the assumption for food inflation have added to the forecast revision by 0.8 points and 0.5 points, respectively. Meanwhile, the stronger-than-projected course in aggregate demand conditions has increased the year-end forecast by 0.3 points through the output gap channel.

The forecasts are based on the assumption that there will be no second wave of pandemic that will require a substantial mobility restriction and no additional deterioration in the global risk appetite. In addition, we assess that the low interest rate environment will last for a long time as advanced and emerging economies maintain their expansionary monetary and fiscal stance. Our projections also rely on an outlook in which maintaining the tight monetary policy stance until the inflation outlook displays a significant improvement and determining the macro policy mix in a coordinated and disinflation-oriented manner will contribute to the improvement in the country risk premium.

I would like to conclude my remarks with a brief evaluation of our recent policies and their impacts on inflation, sustainable growth and macrofinancial stability. In the initial phase of the pandemic, with a primary focus on maintaining the productive capacity of the economy, a comprehensive set of measures was introduced in view of the conditions in that specific period. Expansionary monetary and liquidity policy steps, also backed by financial policies, led to a fast recovery in the economy. However, at this stage, we see that this domestic demand-driven recovery has had significant impacts on inflation and the current account balance. Accordingly, as of early August, coordinated steps have been taken towards normalization in pandemic-specific policies. Through the monetary policy and liquidity management steps I have summarized, we increased the weighted average funding cost by more than 500 basis points. This increase had a strong impact on credit interest rates, and a significant tightening in financial conditions has been achieved. As a result of tightening steps, the credit growth significantly decelerated and a rebalancing started in the import demand.

At this point, containing inflation expectations and restoring the disinflation process as soon as possible are critical for ensuring that growth continues in a sound and stable manner. This requires a tight monetary policy stance until the inflation outlook displays a significant improvement. With the ongoing tightening in monetary and liquidity policies, we predict that inflation will assume a downtrend after the first quarter of 2021. We assess that the improvement to be achieved in the inflation outlook by bringing the real policy rate to positive levels will weaken the dollarization tendency in households’ portfolio preferences. We expect that strengthening the policy coordination with a focus on inflation will contribute to the improvement in macro balances and the disinflation process in the upcoming period.

Distinguished guests,

As I conclude my speech, I would like to thank all my colleagues who contributed to the Report, primarily those at the Research and Monetary Policy Department and the members of the Monetary Policy Committee. I would also like to thank you for your participation.

Finally, I congratulate the October 29th, Republic Day and Mawlid Al-Nabi of our esteemed guests, colleagues and beloved nation.